Advertisement

- Updated on April 16, 2026

- IST 1:26 pm

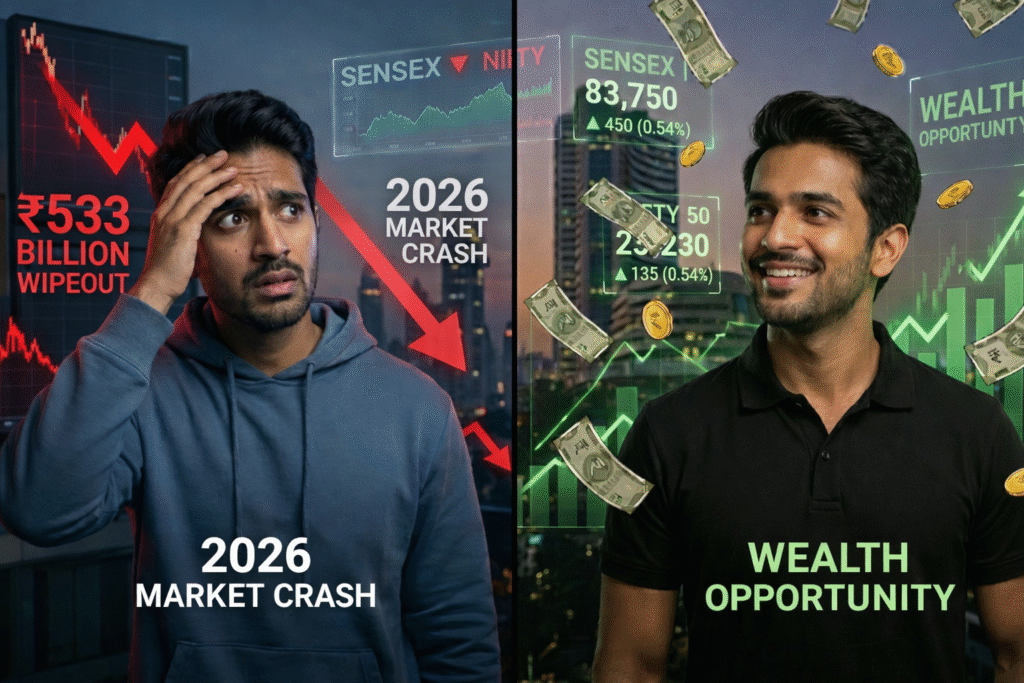

Imagine this: Rahul, a 29-year-old IT professional from Bengaluru, had been riding the bull run since 2023. His portfolio, built through steady SIPs in Nifty index funds, had grown nicely. Then came March 2026. Geopolitical tensions in West Asia spiked oil prices, FIIs pulled out billions, and the markets tanked. In one brutal week, he watched ₹5 lakh vanish from his account. Panicked, he sold everything. “This is the end of the bull run,” he told his wife, booking a loss he still regrets.

Now picture Priya, 27, a marketing executive from Delhi. She too saw the bloodbath—Sensex plunging over 2,000 points in sessions, Nifty dipping below 23,000 at one point. But instead of selling, she did the opposite. She increased her SIP by 20% and deployed a small lump sum into quality large-caps during the dip. “Markets always recover,” she reminded herself, drawing from the 2020 crash lessons her dad shared. Three weeks later, as some stability returned, her portfolio was already showing green shoots. Same crash, two completely different outcomes.

So, what’s the real story behind the ₹533 billion wiped out from India’s market cap in early 2026—the steepest decline in 15 years? Is this the beginning of a prolonged bear market, or the golden buying opportunity Gen Z and millennials have been waiting for? In this blog, we’ll dive deep into the data, expert views from Kotak and Nomura, historical patterns, and practical steps to turn this correction into long-term wealth. Let’s unpack it together, desi style.

Understanding the 2026 Stock Market Crash: What Just Happened?

First, let’s get the basics straight. In early 2026, Indian equity markets witnessed their sharpest erosion in over a decade. Total market capitalization dropped by approximately $533 billion (around ₹44 lakh crore in rupee terms at prevailing rates), marking the worst annual start since 2011. Sensex and Nifty shed 10-15% from their peaks, with intra-day plunges of 1,500-2,700 points triggered by global jitters.

The triggers? A perfect storm. Escalating US-Iran-Israel conflict sent Brent crude soaring past $100-110 per barrel. Foreign Portfolio Investors (FPIs) pulled out over ₹1.27 lakh crore in the first few months—the heaviest outflows in years. Add rising inflation fears, profit booking after a multi-year bull run, and some weak corporate earnings in select sectors. The result? Panic selling, heightened volatility, and valuations cooling from lofty levels.

But here’s the thing: crashes aren’t new to India. We’ve seen 2008, 2013, 2020, and 2022. Each time, the market dipped sharply but recovered stronger for those who stayed invested or bought the fear. For young Indians aged 15-45—many entering the workforce with 20-30 years of horizon—this isn’t a crash. It’s a discount sale on India’s growth story.

The 2026 Crash Explained: Timing, Triggers, and Market Mechanics

Unlike random events, this correction had clear drivers. Oil shock from West Asia tensions directly hit India’s import bill and corporate margins. FII selling intensified as global funds rotated to safer assets amid uncertainty. Domestic institutions (DIIs) and retail investors absorbed some pressure, but the speed of the fall tested nerves.

Rupee weakened to near 94-95 levels against the dollar, adding fuel to the fire for foreign investors. Valuations, which were stretched at 24-25x forward earnings earlier, corrected to more reasonable 20-22x levels—closer to long-term averages.

Think of it like a desi wedding feast turning chaotic midway. The music stops suddenly, guests panic, but the smart ones grab extra servings of the best dishes while prices “correct.” SIP inflows, though slightly moderated to around ₹29,845 crore in February 2026, remained robust, showing retail conviction hasn’t shattered.

The Big Debate: Trap or Your Ticket to Crores?

Here’s where opinions diverge—and rightly so. Let’s weigh both sides fairly.

The Risks – Why It Could Feel Like a Trap

- Prolonged Volatility: If geopolitical tensions linger or oil stays elevated, earnings could take a hit. Nomura recently slashed its December 2026 Nifty target to 24,900, citing near-term risks and possible further 5% correction.

- FII Flows: Sustained outflows could keep pressure on mid- and small-caps, which many young investors favor.

- Emotional Toll: Panic selling during dips has burned many. History shows those who exit rarely time the bottom perfectly.

Take Rahul’s story—he locked in losses and now watches from the sidelines as selective recovery begins.

The Opportunities – Why This Could Be Historic Wealth Creation

- Valuation Reset: Cheaper entry points for quality companies. Kotak Securities maintains a base-case Nifty target of 29,120 by December 2026, with bull-case at 32,032—implying 20-30%+ upside from current levels.

- India’s Structural Strength: Despite the noise, GDP growth remains robust, reforms continue, and domestic consumption is intact. Long-term compounding favors those who buy quality at discounts.

- Historical Precedent: Post-2020 crash, Nifty delivered over 100% returns in the following years for disciplined investors.

Priya’s approach aligns with experts who call this a “buy the dip” moment. Research shows staying invested or adding during corrections has outperformed timing attempts 80% of the time over 10+ year horizons.

The Indian Twist: Crash Meets Our Unique Financial Habits

Fasting during Navratri or Karva Chauth teaches us discipline. Similarly, Indian investors have a cultural edge in weathering storms. We’ve grown up hearing “buy low, sell high” from elders who survived multiple cycles. Yet, many still treat stocks like lottery tickets or FDs.

The beauty? Retail participation via apps like Groww and Zerodha has democratized investing. Young Indians in Tier-2 cities are now active players. Festival bonuses or tax refunds? Instead of gold or fixed deposits that barely beat inflation, smart ones are channeling into SIP top-ups during dips.

Our household savings are shifting from physical assets to equities. This crash tests that shift—but also rewards it for the patient.

Real Stories: Triumphs and Lessons from the 2026 Dip

Let’s hear from real voices navigating this.

- Aarav, 24, Mumbai: A first-time investor who started SIPs in 2024. When markets crashed, he paused his emotions and deployed an extra ₹50,000 in HDFC Bank and Reliance at lower levels. “I treated it like a sale at Big Bazaar,” he laughs. His portfolio is already recovering faster than expected.

- Neha, 31, Hyderabad: A working mom who saw her mid-cap-heavy portfolio drop 18%. Instead of selling, she rebalanced to large-caps and increased SIPs in index funds. “My guru (financial advisor) reminded me: crashes are temporary, compounding is permanent.” She’s now teaching her colleagues the same.

- Vikram, 28, Jaipur: From a conservative family that preferred PPFs. He used the dip to start his first equity SIP. “Bhaiya, maine socha yeh toh 2020 jaisa hai—jo kharida, woh ameer bana.”

These aren’t outliers. Millions of young Indians are quietly accumulating units at bargain prices.

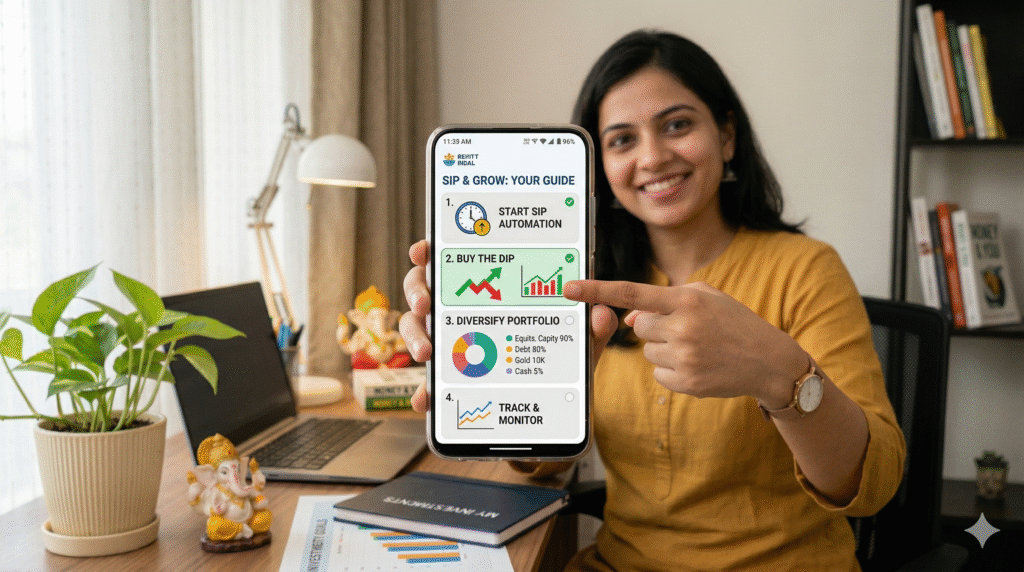

Safe Strategies for the 2026 Crash: Tips to Get It Right

Thinking of acting now? Here’s a balanced, step-by-step playbook:

- Stay Calm and Assess: Don’t check your portfolio daily. Review your goals—retirement, home, education—and risk tolerance.

- SIP is Your Best Friend: Continue or increase existing SIPs. Rupee-cost averaging shines in volatility.

- Buy Quality on Dips: Focus on large-caps, blue-chips with strong balance sheets. Diversify across sectors—banking, IT, renewables, consumption.

- Avoid Panic Selling: History favors long-term holders. If you need money in 1-2 years, keep it in debt funds.

- Rebalance Smartly: Shift from overvalued pockets to undervalued ones.

- Consult Experts: Talk to a SEBI-registered advisor. Personalize your plan—PCOS of investing, if you will.

- Keep Some Dry Powder: Maintain 10-20% in liquid assets for opportunistic buys if it dips further.

Investment Hacks Tailored for Young Indians (15-45)

- Link SIPs to salary day for automation.

- Use goal-based investing: “Dream Bike Fund” or “First Flat Corpus.”

- Top-up during corrections or after bonuses.

- Educate yourself via free AMFI resources or credible YouTube channels.

- Involve family—gift SIP units instead of just cash on birthdays.

- Track macro signals like oil prices and FII flows without obsessing.

Remember: Wealth isn’t made in bull runs alone. It’s built in corrections by the disciplined.

Wrapping It Up: Trap, Opportunity, or Both?

The ₹533 billion wiped out in the 2026 Indian stock market crash isn’t the end of the story—it’s potentially the most exciting chapter yet for patient investors. Yes, risks remain: further volatility, oil shocks, global headwinds. But for India’s young demographic, with decades ahead and structural tailwinds intact, this correction looks more like a launchpad than a dead end.

Experts like Kotak see Nifty heading to 29,000+ by year-end in base case. Nomura, while cautious short-term, still eyes recovery. The choice is yours: panic like Rahul or act strategically like Priya.

If you’re between 15 and 45 and still on the fence, start small today. Even ₹1,000-5,000 monthly SIPs in quality funds during dips can create generational wealth. What’s your move? Did the 2026 crash scare you or excite you? Share your story or first “buy the dip” action in the comments below. Let’s learn from each other and build smarter.

Markets will test you. But disciplined investing rewards you. This isn’t just a crash—it could be your biggest wealth creation opportunity. Stay invested. Stay smart. Your future portfolio will thank you.

You May Like This

Advertisement

You May Like This

Advertisement

Advertisement

Advertisement