Advertisement

- Updated on April 16, 2026

- IST 12:46 pm

Imagine this: Rohan, a 26-year-old software engineer from Pune, followed the “safe” path his parents swore by. Every month, he parked his savings in a fixed deposit at 6.5% interest. Five years later, inflation had quietly eaten away most of his gains. His money grew, but barely kept pace with rising rents and gadget prices. “I thought I was being responsible,” he sighs to his friends over chai. Meanwhile, his colleague Sneha, a 24-year-old marketing executive from Hyderabad, started a simple ₹5,000 SIP in a flexi-cap fund back in college. No fancy stock-picking—just automated monthly investments. Today, her portfolio has grown over 180% in the same period. She’s already eyeing her first home down payment while Rohan is still wondering where his “safe” money went.

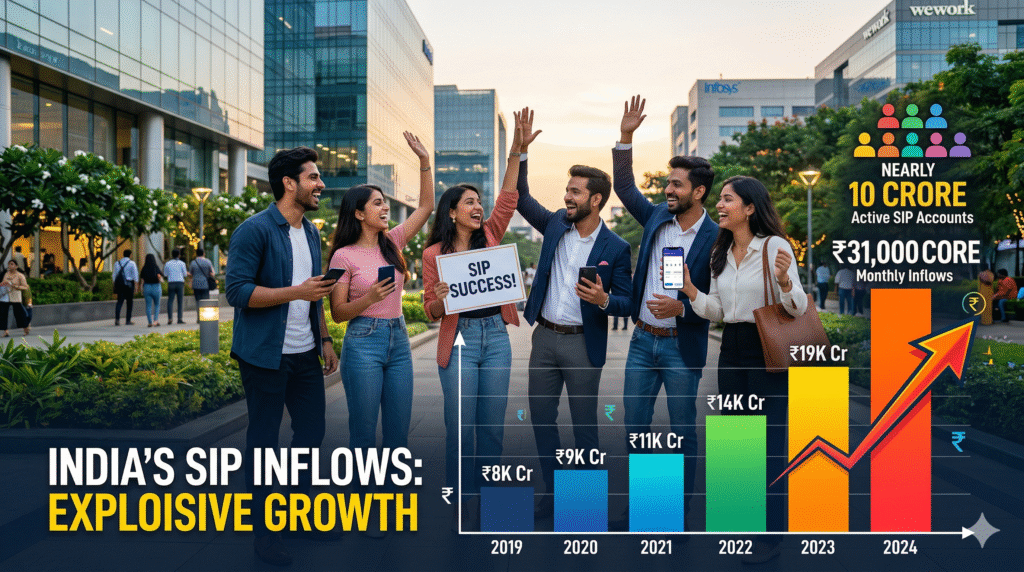

Now picture thousands of young Indians like Sneha. Despite market ups and downs, monthly SIP inflows have smashed records, crossing ₹31,000 crore with nearly 10 crore active accounts. Gen Z isn’t just dipping their toes into investing—they’re diving in headfirst, turning small, consistent steps into massive long-term wealth. Forget the old FD mindset. In this blog, we’ll unpack how automated investing is quietly reshaping India’s financial future, why young investors are shifting from traditional savings to equity mutual funds, and exactly how you can build your own high-growth SIP portfolio. Let’s dive in and see how this silent revolution could make your generation the wealthiest yet.

Understanding SIPs: The Power of Small, Steady Steps

First, let’s break it down simply. A Systematic Investment Plan (SIP) is like a disciplined gym routine for your money. Instead of dumping a lump sum and praying the market timing is perfect, you invest a fixed amount—say ₹1,000 or ₹5,000—every month into mutual funds. It doesn’t matter if the market is high or low; you buy more units when prices dip and fewer when they rise. This magic is called rupee-cost averaging, and it turns market volatility from an enemy into an ally.

Unlike FDs that promise fixed returns but lose to inflation over time, SIPs tap into equity mutual funds that have historically delivered 12-15% compounded annual growth over the long term. Think of it as planting a mango tree: you water it regularly, ignore the seasonal storms, and one day you’re harvesting baskets of fruit. For Gen Z—digital natives juggling EMIs, travel dreams, and side hustles—this automation feels natural. No daily stock watching. Just set it, forget it, and watch compounding do the heavy lifting.

The Record-Breaking Surge: What AMFI Data Reveals in 2026

According to the latest AMFI figures, monthly SIP inflows touched a fresh high of around ₹31,002 crore in recent months, up significantly from previous years. Active SIP accounts hover near the 10-crore mark, with young investors driving nearly 40% of new registrations. This isn’t a flash in the pan. Annual SIP collections crossed ₹3.34 lakh crore in 2025, showing a clear upward trend even amid global volatility.

What’s fueling this? Gen Z’s tech-savvy approach. Apps like Groww, Zerodha Coin, and PhonePe Wealth have made starting a SIP as easy as ordering Swiggy. A quick KYC, bank link, and boom—your first ₹500 is invested. No intimidating bank visits or paperwork hassles that turned off previous generations. This shift marks a massive change in household savings patterns. Indians traditionally parked money in gold, real estate, or FDs. Now, retail investors are channeling savings into equity markets like never before.

Why Gen Z is Ditching FDs for SIPs: The Great Mindset Shift

Let’s talk numbers—because they don’t lie. Over the last 10 years, a disciplined SIP in a large-cap equity fund has delivered around 14% XIRR on average, more than doubling the invested amount in many cases. Compare that to FDs offering 5-7% post-tax returns. A ₹10,000 monthly SIP at 12% over 10 years could grow to roughly ₹23 lakh, while the same in an FD at 6% might reach only ₹16.5 lakh. Over 20 years? The gap becomes life-changing—one crore versus ₹39 lakh.

But it’s not just math. Gen Z has seen their parents’ “safe” savings erode in real terms. Inflation at 5-6% quietly steals purchasing power. Plus, with rising aspirations—owning a bike by 25, a flat by 32, or funding a startup—young Indians want growth, not just preservation. Social media scrolls filled with FIRE (Financial Independence, Retire Early) stories and influencer breakdowns of compounding have normalized investing early. The result? A cultural reset where “risk” is redefined as missing out on wealth creation rather than losing principal.

Of course, not everyone agrees. Some conservative voices still warn about market crashes. Fair point—equity can swing 20-30% in a bad year. Yet history shows staying invested through volatility rewards patience. SIPs excel here because they force you to buy the dip automatically.

The Big Debate: Benefits That Outweigh the Risks

The pros are compelling. First, compounding on steroids. Starting at 22 instead of 35 can mean millions more by retirement. Second, inflation-beating growth. Equity funds have historically outpaced inflation by a wide margin. Third, financial discipline. Automation removes emotion—no panic selling during corrections.

Many Gen Z investors also love the diversification. Flexi-cap, mid-cap, and thematic funds let them back India’s growth story in tech, renewables, and consumption. Research shows young investors are tilting towards equity-heavy portfolios, with 84-95% choosing equity-oriented SIPs on major platforms.

Yet balance demands we acknowledge the cons. Market-linked returns mean no guarantees. A sudden correction can test nerves. Liquidity is good but not instant like FDs. Over-exposure to small-caps (popular among risk-hungry Gen Z) can amplify volatility. The solution? Diversify across large, mid, and flexi-cap funds, and never invest money you’ll need in the next 5 years.

Real-life proof comes from investors who rode the 2020 crash or 2022 correction and emerged stronger. Their SIPs bought cheap units that multiplied when markets recovered.

The Indian Twist: SIPs Meet Desi Financial Habits

Fasting isn’t new to Indians—neither is saving. But our grandparents’ generation relied on gold biscuits, bank lockers, and fixed deposits passed down like family recipes. Today’s Gen Z blends tradition with modernity. Many still gift gold at weddings, but they’re layering SIPs on top for growth. Festival bonuses? Straight into SIP top-ups. First salary? A celebratory SIP setup instead of splurging.

Small-town India is joining the party too. Tier-2 and Tier-3 cities now account for a rising share of new SIP accounts, thanks to UPI and vernacular apps. A young engineer from Lucknow or a teacher from Coimbatore can invest as easily as someone in Mumbai. This democratization is rewriting India’s wealth map.

Real Stories: Triumphs from Young Investors Across India

Let’s hear from the front lines.

- Aarav, 23, Bengaluru: Fresh out of college with a ₹15,000 starting salary, he began a ₹2,000 SIP in a flexi-cap fund. Three years later, even after market dips, his corpus crossed ₹1.2 lakh. “It feels like my future self is high-fiving me every month,” he laughs. He now adds step-up SIPs with every hike.

- Mehak, 28, Mumbai: A content creator who lost money chasing individual stocks in 2022. She switched to SIPs in a balanced hybrid fund. “SIPs taught me patience,” she says. Her portfolio is up 45% in two years, funding her dream Europe trip without debt.

- Vikram, 25, Jaipur: From a traditional family that only trusted FDs and PPF. He started secretly with ₹1,000 SIPs. When he showed his parents the growth chart, they opened their own accounts. “Gen Z is teaching elders now,” he grins.

These stories aren’t outliers. They represent millions quietly building wealth while sipping cutting chai.

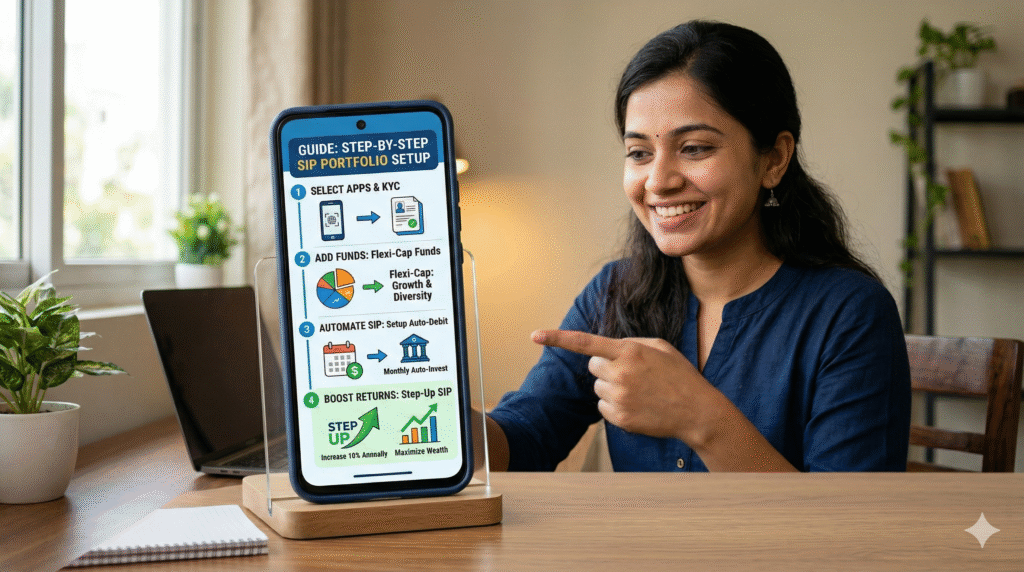

Your Step-by-Step Guide to Starting a High-Growth SIP Portfolio

Ready to join the movement? Here’s how:

- Assess Your Goals: Retirement at 50? Home by 30? Education fund? Define horizon and risk appetite.

- Choose the Right Funds: For young investors (15-35), go 70-80% equity. Top categories: Flexi-cap for balance, large-cap for stability, mid/small-cap for growth (limit to 20-30%). Sample portfolio: 40% Flexi-cap, 30% Large-cap, 20% Mid-cap, 10% Debt/hybrid.

- Pick Amount and Frequency: Start at ₹500-5,000. Use step-up SIPs (increase 10-20% yearly) to match salary growth.

- Use Reliable Apps: Groww, ET Money, or direct AMC portals for zero-commission direct plans.

- Track and Review: Once a year. Rebalance if needed. Avoid frequent tinkering.

- Tax Perks: Equity SIPs held over 1 year qualify for long-term capital gains tax at 12.5% (above ₹1.25 lakh gains). Way better than FD interest taxed as income.

Pro Tips Tailored for Young Indians

- Link SIP to payday for seamless automation.

- Use goal-based SIPs (e.g., “Bike Fund” or “Wedding Corpus”).

- Add lump-sum top-ups during market corrections or bonuses.

- Educate yourself via free resources on YouTube or AMFI site—knowledge compounds too.

- Involve family: Gift SIPs instead of just cash at birthdays.

Wrapping It Up: Your Turn to Build Generational Wealth

SIPs hitting ₹31,000 crore monthly isn’t just a statistic—it’s proof that Gen Z is rewriting India’s wealth narrative. By choosing automation over guesswork, equity over guaranteed mediocrity, and consistency over timing, young Indians are positioning themselves as the richest generation yet. The shift from FDs to SIPs isn’t hype; it’s a calculated, data-backed move toward financial freedom.

If you’re 15-45 and still sitting on the sidelines, start small today. Even ₹1,000 monthly can snowball into serious wealth over 15-20 years. What’s stopping you? Drop your SIP story or first-investment plan in the comments below. Let’s inspire each other and turn this quiet revolution into a nationwide movement. Your future self (and maybe your kids) will thank you.

Remember: Wealth isn’t about luck. It’s about starting now, staying consistent, and letting time do its magic. Forget FDs. Embrace SIPs. Become the richest version of yourself.

You May Like This

Advertisement

You May Like This

Advertisement

Advertisement

Advertisement