Advertisement

- Updated on April 16, 2026

- IST 1:50 pm

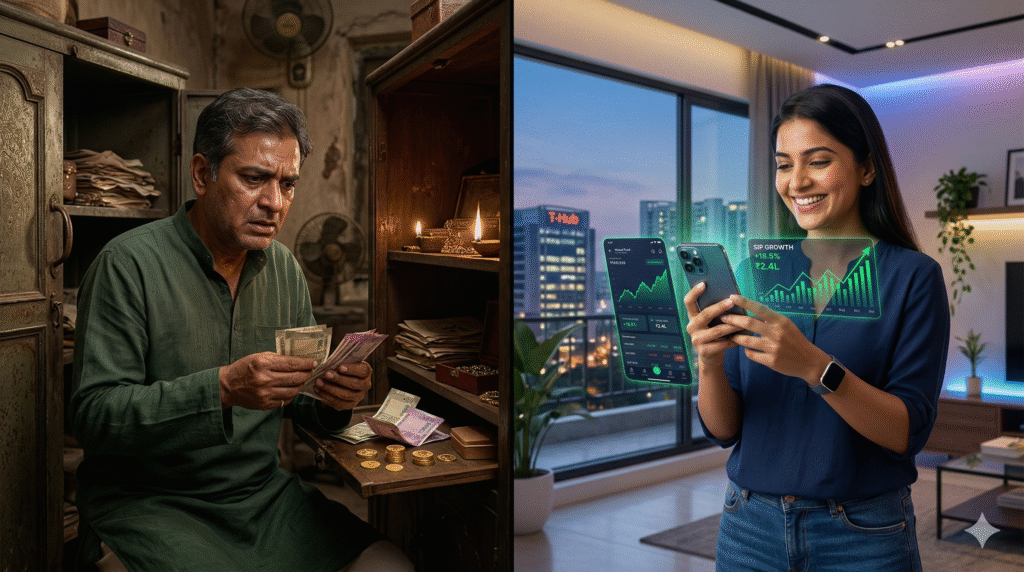

Imagine this: Rajesh, a 42-year-old shopkeeper from Lucknow, has always played it safe. Every extra rupee goes into a shiny gold chain for his daughter’s wedding or a fat fixed deposit that promises “guaranteed returns.” Cash stays tucked in the almirah, just in case. But after five years of watching inflation nibble away at his savings like a silent thief, his “safe” pile barely keeps pace with rising prices. His dreams of a comfortable retirement feel stuck in neutral.

Now picture Meena, a 29-year-old software engineer from Hyderabad. She too grew up hearing stories of gold as the ultimate security. But last year, inspired by friends and a simple app on her phone, she started small SIPs in mutual funds and blue-chip stocks. No drama, just steady monthly transfers from her salary. Today, her portfolio has grown by nearly 40% in two years—enough to fund a down payment on a small flat while still leaving room for family vacations. For her, the old ways feel like yesterday’s news.

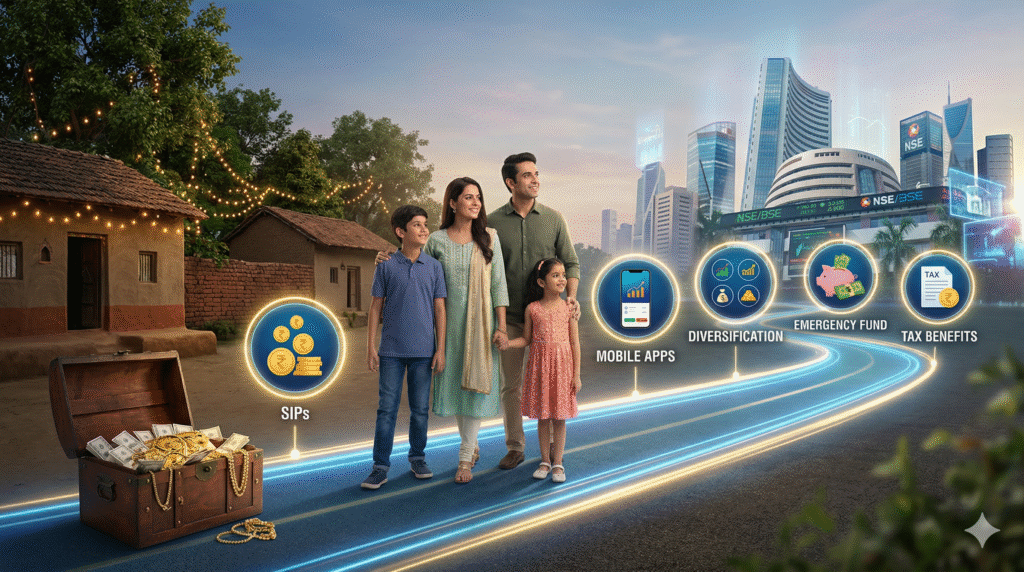

So, what’s the real story? Is the traditional Indian love affair with cash, gold, and fixed deposits finally fading? The Economic Survey 2025-26, tabled just before Budget 2026, has dropped a bombshell: Indian households are quietly but dramatically shifting their savings away from cash, bank deposits, and even gold toward shares, mutual funds, and pension plans. This isn’t a fleeting trend—it’s a structural reset in how we build wealth. In this blog, we’ll unpack the data, explore the “why” behind this cash-to-equity revolution, weigh the risks and rewards, share real Indian stories, and give you a practical blueprint to rebalance your own portfolio. Whether you’re a college student just starting out or a mid-career parent juggling EMIs, this shift could be your ticket to smarter money moves in 2026 and beyond.

Understanding the Shift: The Numbers That Tell the Real Story

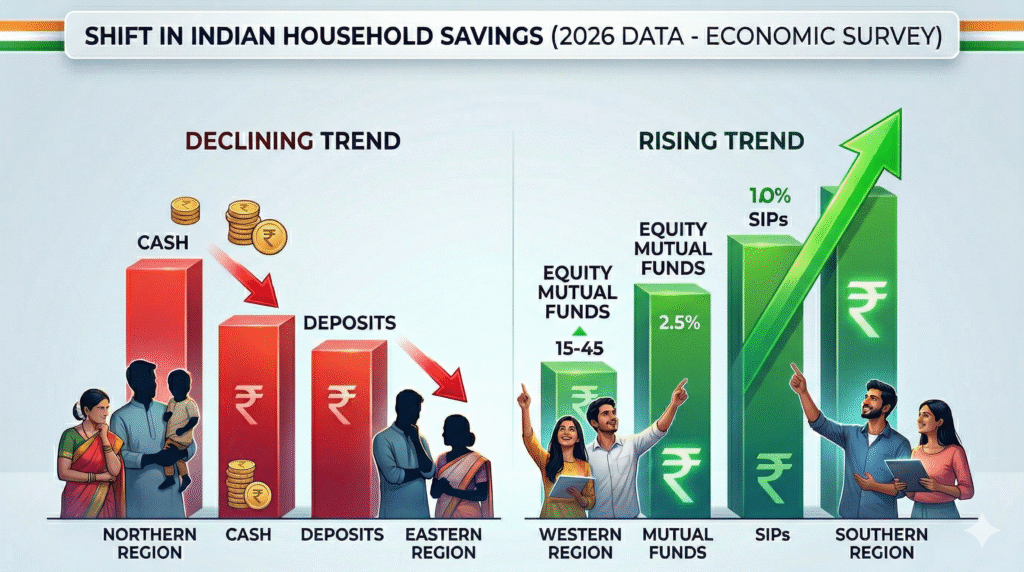

Let’s cut through the jargon and look at the hard facts straight from the Economic Survey 2025-26. The share of equity and mutual funds in annual household financial savings has skyrocketed from a mere 2% in FY12 to over 15.2% in FY25. That’s not a blip—it’s a seven-fold leap in systematic investment plan (SIP) contributions, with average monthly flows jumping from under ₹4,000 crore in FY17 to more than ₹28,000 crore by November 2025.

Meanwhile, the old reliable—bank deposits—has seen its dominance shrink dramatically. Its share in household savings has dropped from nearly 58% in FY12 to around 35% in FY25. Even currency and cash holdings have taken a hit, falling from over 12% to under 6% of savings flows. Household equity wealth alone swelled by a staggering ₹53 lakh crore between April 2020 and September 2025, pushing individual equity holdings to roughly ₹84 lakh crore.

Gold? It’s still a cultural heavyweight—Indian households hold an estimated $5 trillion worth—but the incremental savings are clearly flowing elsewhere. Real estate remains a big part of overall wealth (often 50-60% for many families), yet even there, the buzz is shifting toward financial assets that offer liquidity and growth without the hassle of property maintenance or illiquidity.

Budget 2026 builds on this momentum with subtle nudges: incentives for municipal bonds, tweaks to make equity investing more accessible for NRIs, and a broader push for capital market deepening. The hidden signal? India’s households are no longer just savers—they’re becoming investors. This “financialisation” of savings is reshaping everything from bank liquidity to stock market participation.

Why Indian Households Are Making the Leap: The Perfect Storm

Think of it like this: for decades, cash and gold were the safety nets in an uncertain economy. Gold glittered during weddings and festivals; fixed deposits felt as secure as a family vault. But times have changed. Inflation, even when moderated, has quietly eroded real returns on traditional instruments. Post-tax FD yields often struggle to beat 6-7% inflation-adjusted growth, while equity markets—powered by India’s 7%+ GDP trajectory—have delivered compounded double-digit returns over the long haul.

Fintech has been the game-changer. Apps like Groww, Zerodha, and PhonePe have turned investing into something as simple as ordering chai via Swiggy. Demat accounts have exploded—over 18% of NSE market cap is now held by retail investors, a 22-year high. Young Indians (15-45, exactly our audience) are leading the charge: digital natives who saw their parents’ savings stagnate during the pandemic and decided enough was enough.

Other drivers? Rising financial literacy through social media, YouTube explainers, and workplace webinars. Pension and provident fund contributions have also climbed (from 16.6% to 22.2% of savings), showing a smart blend of safety and growth. Even cultural shifts play a role—nuclear families, dual-income households, and aspirational spending mean people want their money to work harder, not just sit idle.

Of course, it’s not all rosy. Higher household debt (now 41.3% of GDP) signals some are borrowing to consume or invest, raising eyebrows about sustainability. Yet the Survey calls this a “structural shift,” not speculation. Markets have rewarded patience: mutual fund AUM crossed ₹80 lakh crore, with retail folios at record highs.

The Big Debate: Blessing or Hidden Risk?

Like any big change, this cash-to-stocks move sparks debate. Let’s weigh both sides fairly.

The Pros: Why Stocks and MFs Are Winning Hearts

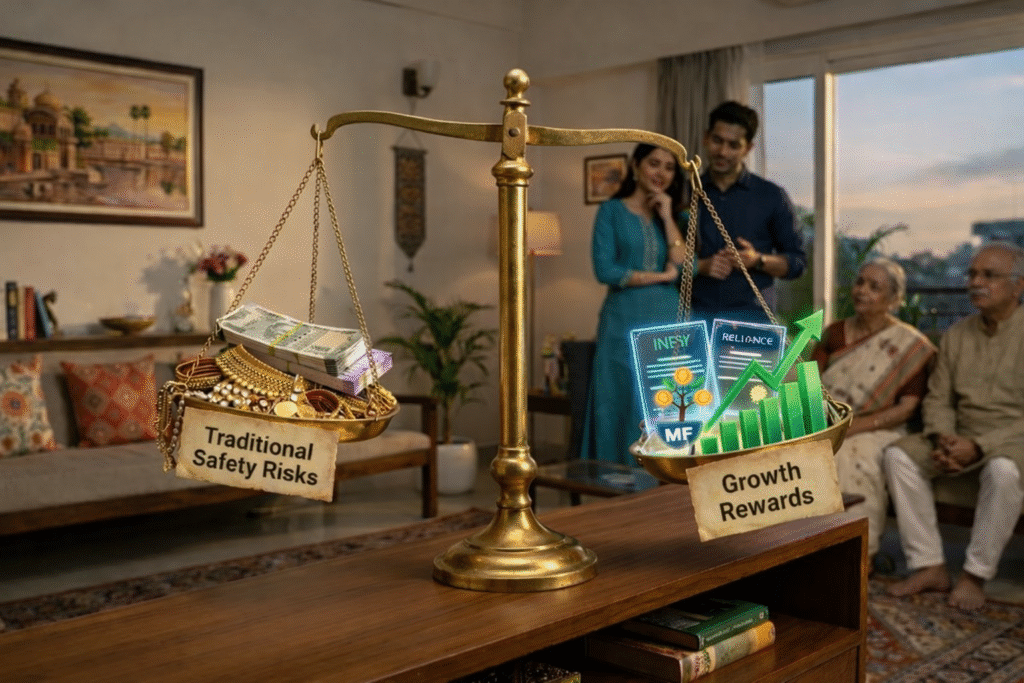

- Superior Wealth Creation: Equities have historically outpaced gold and FDs over 10+ year horizons. That ₹53 lakh crore equity wealth surge isn’t luck—it’s compounding at work.

- Inflation Hedge with Growth: Unlike fixed deposits that lose steam after tax, diversified MFs and stocks ride India’s growth story—think IT, renewables, manufacturing.

- Liquidity and Accessibility: Sell a stock in seconds; redeem an MF overnight. No waiting for property buyers or melting gold.

- Tax Efficiency: Long-term capital gains (over 12 months) at 12.5% (with indexation benefits in some cases) beat many traditional options post-Budget tweaks.

Meena’s story isn’t unique—millions of SIP investors have seen their money grow while building emergency funds separately.

The Cons: Where Caution Is Still King

- Volatility Bites: Markets can crash 20-30% in bad years. Not everyone has the stomach (or timeline) for it.

- Emotional Traps: Panic-selling during corrections undoes years of gains. The Survey notes retail participation spiked but so did selectivity.

- Opportunity Cost on Gold: Cultural gold hoarding still locks away massive capital ($5T+). It shines in crises but lags in bull markets.

- Debt Overhang: Some households are leveraging up—credit card spends and personal loans are rising. Over-investing without an emergency buffer could backfire.

The balanced view? This shift works best for those with a 5-10+ year horizon, diversification, and professional advice. It’s not “dump everything into stocks tomorrow”—it’s smart rebalancing.

The Indian Twist: Tradition Meets Fintech Revolution

Fasting during Navratri or Karva Chauth is cultural muscle memory for us Indians—gold and cash were once the same. Weddings, festivals, and “khaata-peeta” family values screamed physical assets. Yet 2026 India is different. Gen Z and millennials in Tier-2 cities like Lucknow, Kochi, or Guwahati are using UPI and apps to invest ₹500 SIPs while sipping cutting chai.

Real estate? Still loved for status, but RERA transparency and high stamp duties make it less appealing for quick wealth. Gold loans have boomed, but many are now using gold as collateral to fund equity investments—a clever hybrid.

The Survey hints this financialisation supports broader goals: more capital for infrastructure, startups, and jobs. Budget 2026’s bond market pushes and SME funds aim to channel this energy productively.

Real Stories: Triumphs, Tumbles, and Turning Points

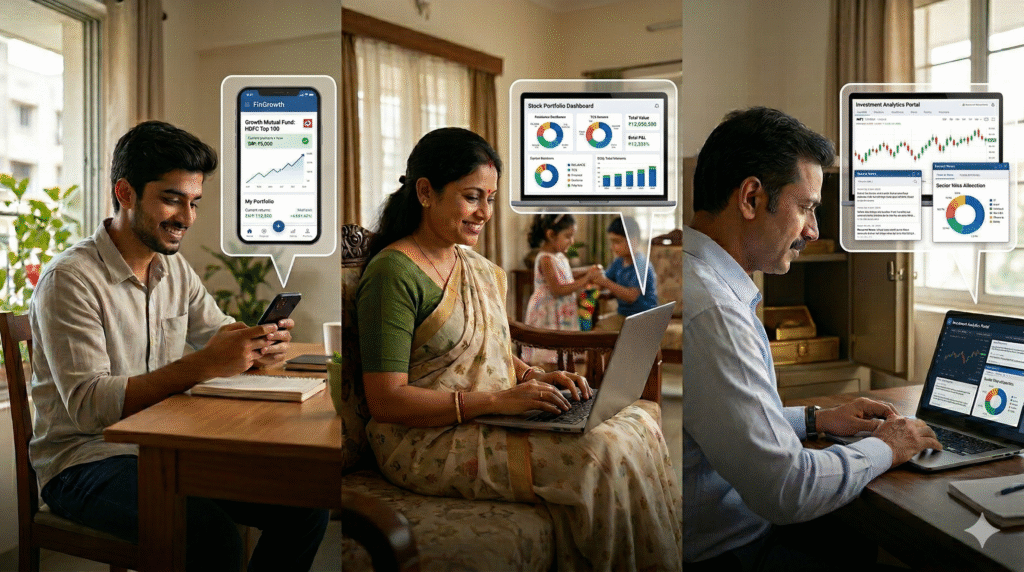

- Aarav, 24, Pune: Fresh out of engineering college, he ignored his dad’s advice to “buy gold” and started a ₹1,000 monthly SIP in an index fund. Two years later, it’s up 35%. “Dad still keeps some gold, but even he opened a demat account after seeing my returns,” he laughs.

- Priya, 38, Kolkata: A working mom who lost money in 2022’s correction by going all-in on stocks. She paused, diversified into hybrid MFs and PPF, and is now back on track. “Lesson learned: don’t chase trends—build steadily.”

- Vikram, 45, Chennai: Traditional businessman who shifted 30% of his cash reserves into pension plans and blue-chip stocks after the Survey headlines. His family business is thriving, but he says, “Gold is for security; stocks are for my kids’ future.”

These aren’t outliers. From Mumbai’s dabbawalas discussing SIPs to Delhi’s auto drivers checking apps during breaks, the change is grassroots.

Blueprint for Rebalancing: Safe Steps to Join the Shift

Ready to move beyond cash and gold? Here’s a practical, India-friendly roadmap:

- Assess Your Current Mix: List assets—cash, FD, gold, real estate, stocks/MFs. Aim for 40-60% equities (depending on age/risk) over time.

- Start Small and Systematic: Begin with ₹500-1,000 SIPs in diversified equity MFs or index funds. Use tax-saving ELSS for dual benefits.

- Keep an Emergency Buffer: 6-12 months’ expenses in liquid funds or savings—not all in stocks.

- Diversify Smartly: Blend large-cap, mid-cap, debt, and gold ETFs. Consider Sovereign Gold Bonds for tax-free gold exposure.

- Leverage Tax and Pension Perks: Max out NPS contributions (extra deduction under 80CCD) and use Budget-friendly bond incentives.

- Stay Educated, Seek Help: Track via apps, read SEBI-approved resources, consult a certified advisor. Review annually.

- Mind the Debt: Pay high-interest loans first before aggressive investing.

Desi Investment Hacks for 2026

- Pair SIPs with salary credits for “set-and-forget” discipline.

- Use festive seasons (Diwali, Akshaya Tritiya) for lump-sum top-ups in dips.

- Teach kids via junior demat accounts—start early compounding.

- Avoid FOMO: Ignore “hot tips” on WhatsApp; stick to fundamentals.

Wrapping It Up: Cash Is Dead—Long Live Smart Investing?

Budget 2026’s hidden signal is clear: Indian households are voting with their wallets for growth over mere safety. Dumping excess cash and underperforming gold for stocks and MFs isn’t reckless—it’s realistic in a booming economy. For some, it’s life-changing wealth creation. For others, poor execution could sting. The difference? Discipline, knowledge, and patience.

The choice is yours. Start small today—open that demat account, set up your first SIP, or simply audit your portfolio. What’s your money story? Are you still team gold-and-FD or have you joined the equity wave? Drop your experiences in the comments below—let’s learn from each other and build smarter financial futures together. Your wealth journey starts now. Share this with a friend who needs the nudge!

You May Like This

Advertisement

You May Like This

Advertisement

Advertisement

Advertisement