Advertisement

- Updated on April 16, 2026

- IST 4:39 pm

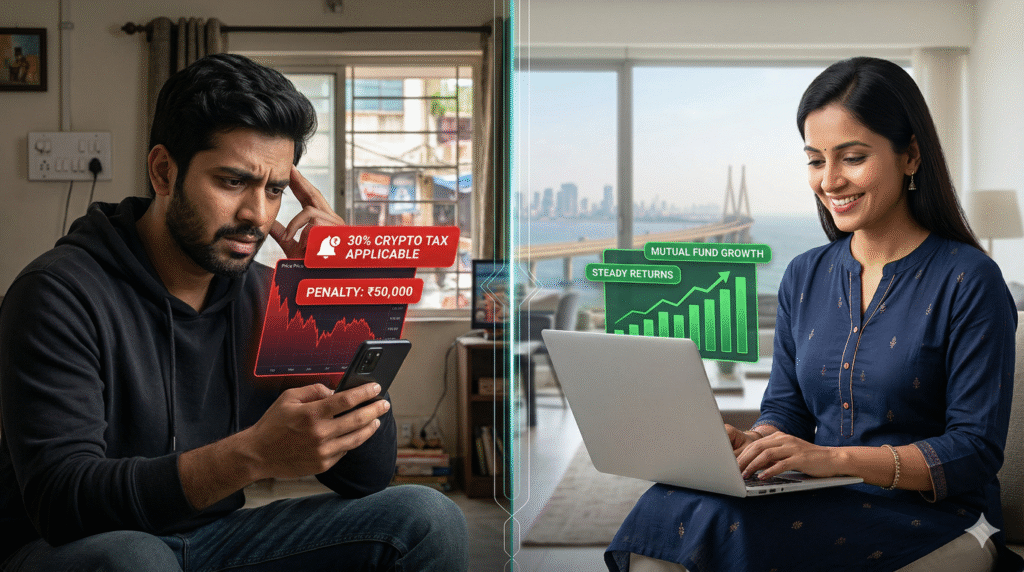

Imagine this: Rahul, a 27-year-old software developer from Bangalore, rode the 2025 Bitcoin wave like a pro. He bought low on a popular Indian exchange, watched his portfolio surge 180%, and cashed out what felt like life-changing gains. “This is it—early retirement vibes!” he told his friends over filter coffee. But come tax filing season, the 30% flat tax on his Virtual Digital Asset (VDA) profits wiped out nearly a third of his winnings. Worse, a small reporting glitch on the exchange side triggered a ₹50,000 penalty notice under the new Budget 2026 rules. His “easy money” turned into a stressful audit nightmare, leaving him drained and swearing off crypto forever.

Now picture Priya, 32, a marketing executive from Mumbai. She too dabbled in crypto but approached it differently—small, compliant trades only, with meticulous records. When the same tax rules hit, she crunched the numbers and pivoted most of her savings into mutual funds and index stocks. Six months later, her portfolio is growing steadily without the penalty headaches or sleepless nights over volatility. For her, skipping the crypto frenzy feels like the smartest move of her financial life.

So, what’s the truth? With Budget 2026 retaining the brutal 30% tax on crypto gains and slapping on strict new penalties for non-reporting, is crypto still worth touching in India in 2026? For young Indians chasing quick wealth in a digital-first world, the allure remains—but the math has never looked harsher. In this blog, we’ll break down the exact rules, weigh the real risks against any remaining rewards, share gritty real-life stories from Indian traders, and offer practical tips plus smarter alternatives rooted in our desi financial reality. Whether you’re a college student eyeing your first investment or a mid-20s professional juggling EMIs, let’s figure out if crypto still belongs in your 2026 portfolio. Let’s dive in.

Understanding Virtual Digital Assets: The Tax Net Tightens

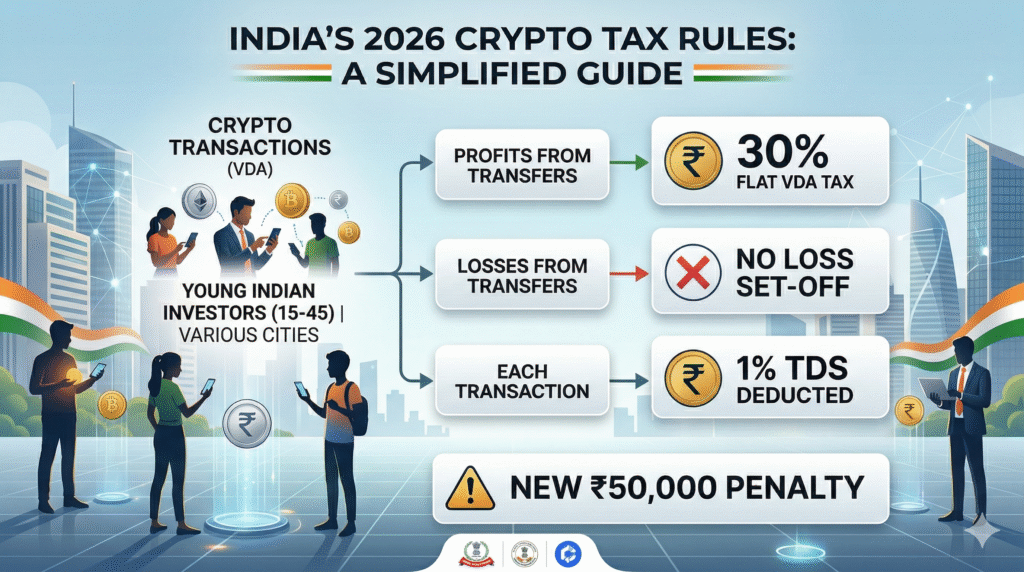

First, let’s get the basics crystal clear. Virtual Digital Assets (VDAs) cover pretty much everything crypto-related—Bitcoin, Ethereum, altcoins, NFTs, and even certain tokens. Since 2022, India has treated them under a special tax regime that’s one of the world’s toughest. Budget 2026? No major relief. The 30% flat tax stays put, the 1% TDS on transfers continues, and new compliance hammers have been added to crack down on sloppy reporting.

Think of it like this: your crypto profits aren’t treated as regular income or even normal capital gains. They fall under Section 115BBH of the Income Tax Act—no slab benefits, no indexation, and almost zero deductions except the original cost of acquisition. Add 4% health and education cess, and your effective hit often crosses 31.2%. Losses from one coin can’t offset gains from another. Sell at a loss? Tough luck—you eat it fully while still paying tax on winners.

The 1% TDS (under Section 194S) kicks in on most transfers above ₹10,000–50,000 thresholds (depending on your status). Exchanges deduct it upfront, so you feel the pinch immediately. And now, from April 1, 2026, the new penalty provisions under the updated Section 446 make non-compliance expensive. Reporting entities (exchanges, wallets) face ₹200 per day for delayed statements and a flat ₹50,000 for inaccurate info or failure to fix errors. While aimed at platforms, the ripple effect hits retail users—delayed filings, audits, or even frozen accounts if things go south.

This isn’t just paperwork; it’s a deliberate push for traceability in a space once seen as wild west. The government wants data, not speculation. For the average 15-45-year-old Indian—tech-savvy, ambitious, but often juggling student loans or home EMIs—this regime turns “high-reward” into “high-headache.”

Crypto Taxation Explained: Timing, TDS, and the New Penalty Trap

Let’s break it down without the jargon overload. You transfer crypto (buy, sell, swap, or even gift in some cases)—1% TDS gets deducted if it crosses the limit. Later, when you file ITR, you report the full gain and pay 30% flat tax on it. No long-term vs short-term benefit. No setting off against salary or other income except specific VDA losses in rare cases.

The fresh Budget 2026 twist? Stricter reporting under Section 509. Exchanges must now file detailed transaction statements. Miss the deadline or mess up the data? Daily ₹200 fines pile up, and a ₹50,000 one-time penalty lands for inaccuracies. Many young traders I’ve heard from worry this could indirectly affect them—if your exchange slips up, you’re the one explaining it to the taxman during assessment.

Compare that to traditional investments: equity mutual funds or stocks enjoy 12.5% LTCG tax (after one year, with exemptions up to ₹1.25 lakh). Fixed deposits? Taxed at your slab but predictable. Real estate? Indexation benefits in many cases. Crypto stands alone in its punitive corner.

The Big Debate: Crypto in 2026 – High Risk or Hidden Opportunity?

Here’s where opinions split sharply among experts, traders, and financial advisors. Let’s look at both sides honestly.

The Pros: Why Some Still Dip Their Toes

- Explosive Upside Potential: Despite taxes, global crypto cycles can deliver 5x–10x returns in bull runs—something hard to match in Indian stocks or MFs consistently.

- Diversification and Global Exposure: For young Indians tired of rupee volatility, Bitcoin or Ethereum offers a hedge against inflation and currency risks.

- Tech and Innovation Play: NFTs, DeFi, and blockchain projects align with India’s startup culture—many 20-somethings see it as backing the future of finance.

- Ease of Entry: Apps make it feel like ordering Zomato—low barriers for the 15-45 crowd glued to phones.

Some disciplined traders still net positive after tax by timing entries smartly and treating it as a small “satellite” portfolio (5-10% allocation).

The Cons: Why Most Advisors Say “Proceed with Extreme Caution”

- Tax Erosion Kills Profits: That 30% + cess + TDS means you need massive gains just to break even after costs. A 50% return pre-tax shrinks dramatically.

- Volatility + No Loss Set-Off: Market crashes hurt twice as hard—you absorb full losses while paying full tax on any winners.

- Compliance and Penalty Risks: The new ₹50,000 penalty and daily fines create anxiety. One missed form or exchange error, and your gains vanish into fines.

- Opportunity Cost: Money locked in crypto could grow more tax-efficiently in equity MFs, NPS, or even PPF—options with better long-term compounding for retirement dreams.

- Regulatory Uncertainty: While no ban, the message is clear: government wants control, not encouragement.

For most middle-class Indian households, the cons outweigh the pros unless you’re a full-time trader with iron discipline and deep pockets.

The Indian Twist: Crypto Meets Desi Reality and Regulations

Crypto isn’t new to our cultural DNA—we love high-risk bets during festivals like Diwali or Akshaya Tritiya. But in 2026 India, it clashes with our love for “safe” assets like gold, FDs, and real estate. Young urban professionals in Tier-1 and Tier-2 cities (Bangalore, Hyderabad, Pune) drove the 2021–22 frenzy, but post-tax reality has cooled many.

Nuclear families, rising EMIs, and parental pressure for “stable” wealth building make the penalty risk feel extra heavy. Plus, with UPI and fintech making stocks and MFs ridiculously easy, why battle 30% tax when SIPs in Nifty 50 deliver solid 12-15% annualized with friendlier rules?

The Budget’s focus on reporting also signals India’s push to formalize the economy—great for the nation, but a speed bump for retail crypto dreams.

Real Stories: Triumphs, Tumbles, and Tough Lessons

Let’s hear from folks who’ve lived it.

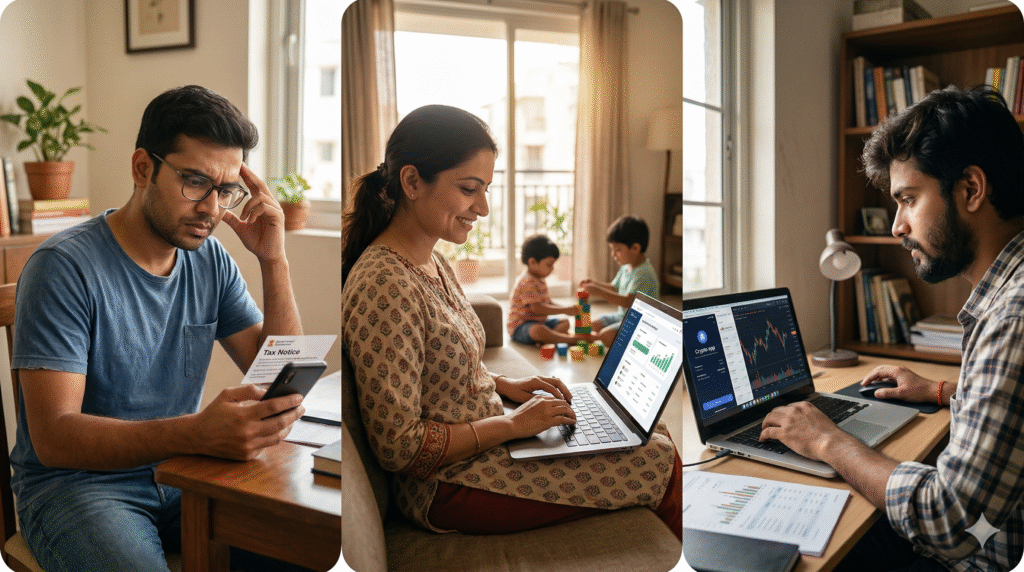

- Arjun, 24, Delhi: Started with ₹20,000 in altcoins during a dip. Made 300% on paper but lost 40% after tax and TDS. “Felt like the government took my bonus,” he laughs now. Switched to index funds—happier and sleeping better.

- Sneha, 31, Chennai: Treated crypto as 8% of her portfolio with strict stop-losses. Cleared taxes on time and still profited modestly. “It’s possible if you treat it like a side hustle, not a lottery ticket,” she shares.

- Vikram, 28, Kolkata: Hit with a ₹50,000 penalty after an exchange reporting delay in early 2026. “Lost more in fines than I made that quarter.” Now he sticks to mutual funds and laughs about his “crypto phase.”

These stories show one thing: crypto isn’t a magic wand. It’s a high-stakes tool—how (and if) you use it matters hugely.

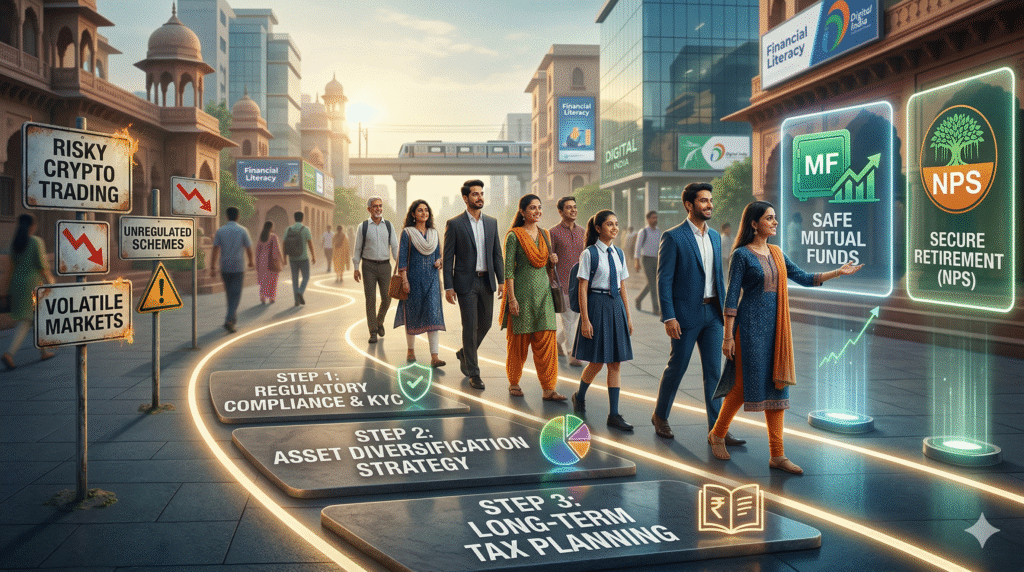

Safe Crypto Strategies (or Smarter Alternatives): Tips to Protect Your Wallet

Thinking of staying in or dipping in anyway? Here’s how to play it smart—or know when to walk away:

- Size It Tiny: Limit crypto to 5% max of your portfolio. Never invest money you can’t afford to lose entirely.

- Track Everything: Use apps or Excel for cost basis, TDS certificates, and transaction logs. File ITR-2 or ITR-3 carefully.

- Choose Compliant Platforms: Stick to registered Indian exchanges with good reporting track records to minimize penalty risks.

- Time Your Taxes: Plan exits around your overall tax slab. Consider gifting or other structures only after expert advice.

- Hybrid Approach: Pair small crypto exposure with tax-efficient assets like ELSS funds or NPS for balance.

- Consult Pros: Talk to a CA or SEBI-registered advisor familiar with VDA rules. Don’t DIY complex filings.

- Know When to Exit: If the stress outweighs rewards, shift to equity MFs, sovereign gold bonds, or international stocks via mutual funds.

Desi Investment Hacks: Crypto vs Mutual Funds, Stocks & More in 2026

What should replace or complement crypto? Here’s a quick 2026-friendly comparison for Indian youth:

- Equity Mutual Funds/Index Funds: 12.5% LTCG after one year, ₹1.25 lakh exemption—far kinder than 30%.

- NPS Tier-1: Tax deductions up to ₹50,000 extra + market-linked growth with lock-in discipline.

- Direct Stocks via Apps: Same LTCG benefits + ownership thrill without crypto volatility.

- Gold ETFs/SGBs: Tax-efficient cultural favorite with lower risk.

Hack: Automate SIPs on salary day, use festive dips for lump sums, and review quarterly. Teach younger siblings via junior accounts—build generational wealth the smart way.

Wrapping It Up: To Touch Crypto or Not in 2026?

Budget 2026’s message on crypto is loud and clear: 30% tax, 1% TDS, and ₹50,000 penalties for reporting lapses make it a high-friction, high-tax gamble. For some disciplined, risk-loving Indians, a tiny slice can still spark excitement and occasional outsized wins. For most 15-45-year-olds building real-life goals—home, marriage, kids, retirement—the numbers simply don’t add up when safer, tax-friendlier options deliver steadier growth.

Crypto isn’t “dead,” but it’s no longer the effortless side hustle many hoped for. The brutal truth? In 2026 India, smart wealth creation favors discipline over speculation. Audit your portfolio today, talk to a professional, and align with the new reality.

What’s your take? Still holding crypto despite the tax bite, or have you shifted to mutual funds and stocks? Drop your story in the comments below—let’s swap notes, learn from each other, and build smarter financial futures together. Share this with a friend who’s still on the fence. Your wallet will thank you!

You May Like This

Advertisement

You May Like This

Advertisement

Advertisement

Advertisement