Advertisement

- Updated on April 17, 2026

- IST 2:51 am

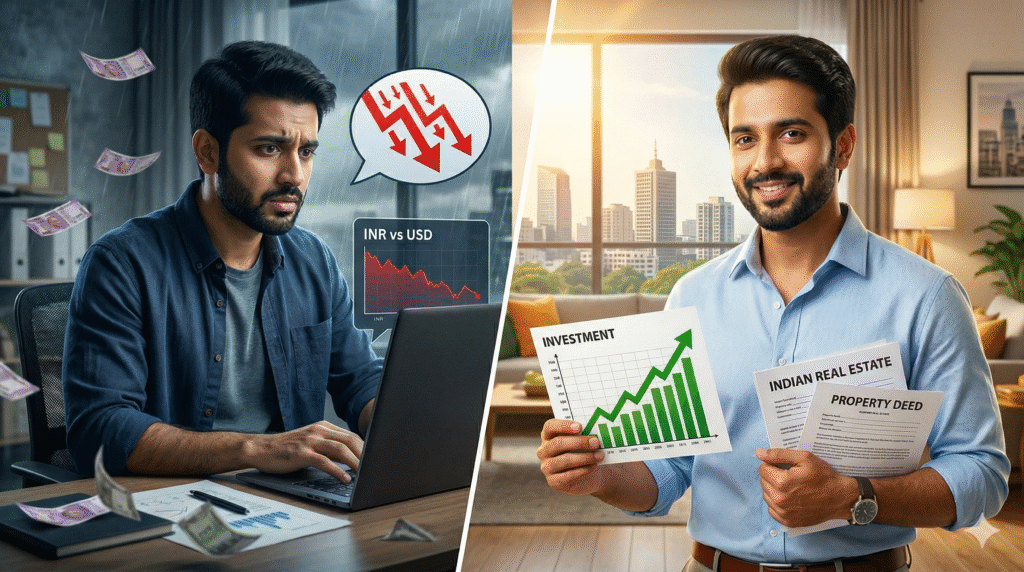

Imagine this: Vikram, a 35-year-old software engineer from Bengaluru now living in Dubai, had carefully built a portfolio of Indian mutual funds and blue-chip stocks over the last five years. His investments grew a solid 14% in rupee terms last year—impressive on paper. But when he needed funds for his daughter’s education back home and converted everything to dollars in early 2026, the shock hit hard. The rupee had slid from around 83 to nearly 93 against the dollar amid soaring oil prices and global jitters. His “gains” evaporated into a net loss in real dollar terms. “I thought I was securing my family’s future,” he confided to a friend over a video call, “but the falling rupee turned my smart moves into a silent wealth drain.”

Now picture Meena, 42, an NRI banker in London. She faced the same rupee slide but took a different path. Instead of panicking, she ramped up remittances during the dip, bought into Indian real estate at what felt like a discount, and hedged part of her equity exposure through smart currency tools. Six months later, her family’s new apartment in Pune is appreciating, her dollar remittances stretched further in India, and her overall returns held steady. “The rupee storm actually became my opportunity,” she says with a smile.

So, what’s the real story here? Is the falling rupee in 2026 a curse that’s quietly eating into NRI and FPI profits, or could it be a disguised blessing if you play it right? With elevated oil prices triggered by Middle East tensions and brokerages like Bernstein downgrading Indian equities over macro risks, the pressure on the Indian rupee is real. In this blog, we’ll unpack exactly how rupee depreciation 2026 is reshaping NRI investment India returns, driving FPI outflow India trends, and what currency risk management looks like for everyday investors. We’ll explore fresh angles, real experiences from the Indian diaspora, and practical hedging strategies India that can protect your hard-earned wealth. Let’s dive in and turn confusion into clarity.

Understanding the Falling Rupee: A 2026 Economic Storm

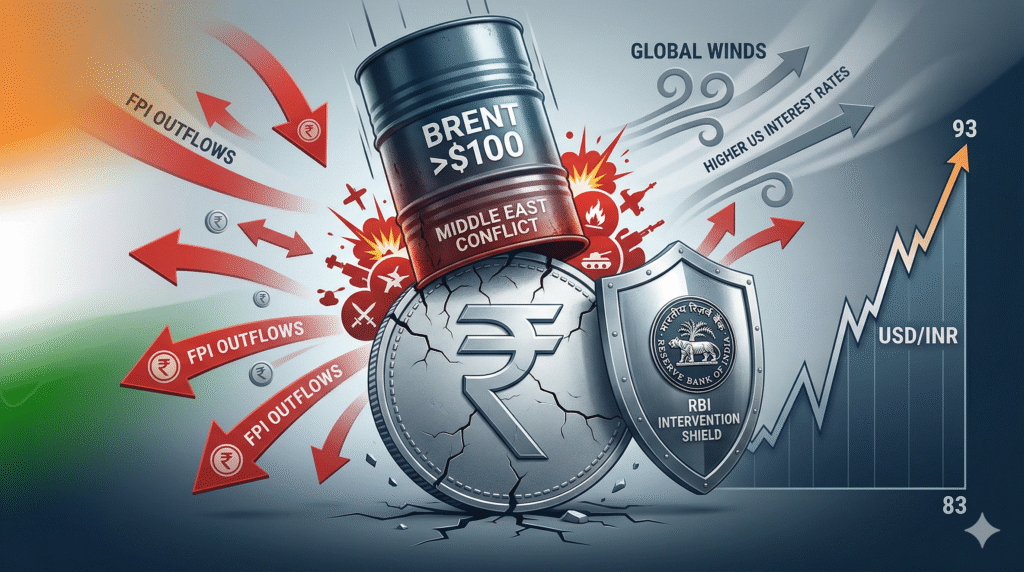

First, let’s demystify what’s happening. The Indian rupee isn’t just “falling”—it’s navigating a perfect storm of global headwinds. By April 2026, the USD/INR pair has hovered near record highs around 92-95, marking one of the sharpest depreciations in recent memory—roughly 8-9% over the past year in some stretches.

Think of the rupee like a boat in choppy seas. On one side, India’s heavy reliance on oil imports (over 80% of needs) means every spike in crude prices punches the currency hard. The ongoing Iran-related tensions pushed Brent crude well above $100-110 per barrel at points, inflating import bills and widening the current account deficit. On the other side, foreign portfolio investors (FPIs) have pulled out massive sums—over ₹1.27 lakh crore in early 2026 alone, with March seeing a record monthly outflow. This sell-off, combined with global uncertainties like US trade policies and shifting interest rates, created a feedback loop: outflows weaken the rupee, which makes India less attractive, triggering more outflows.

RBI has stepped in with FX curbs, tighter rules on bank positions, and interventions to stabilize things, but the pressure lingers. For the average Indian family with overseas ties, this isn’t abstract economics—it’s personal. Whether you’re an NRI sending money home or an FPI allocating capital, the INR vs USD gap directly hits your pocket.

How Rupee Depreciation Hits NRI Investments: From Remittances to Real Returns

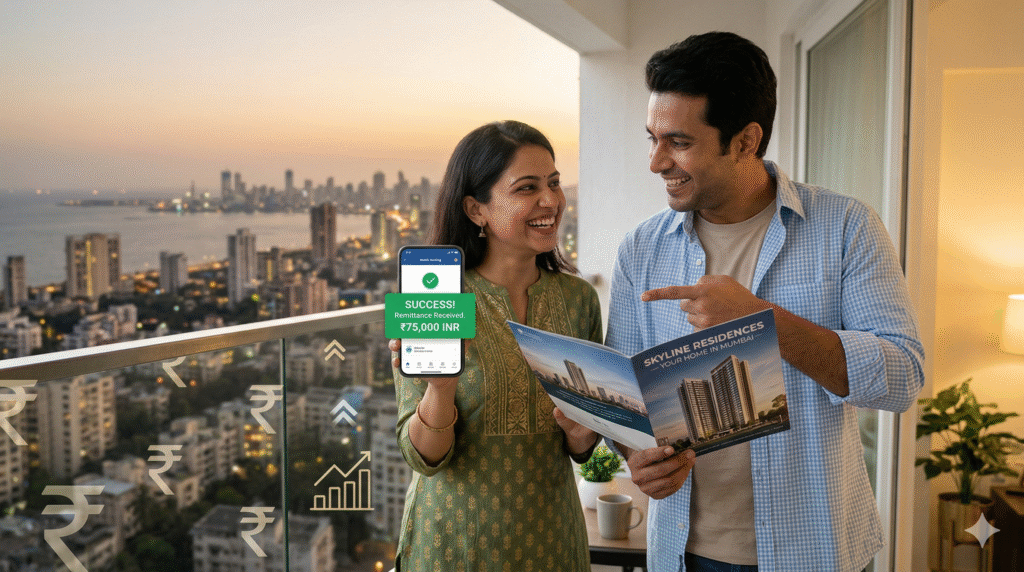

For NRIs, the story splits into two sides of the same coin. On the bright side, a weaker rupee makes remittances more powerful. If you earn in USD, GBP, or AED, each unit now buys more rupees—perfect for supporting family, funding education, or building an emergency fund back home. Many NRIs reported a surge in transfer volumes in 2026 precisely because their foreign currency stretched further in India’s desi markets.

But here’s the catch that many overlook: when it comes to NRI investment India in equities, mutual funds, or even fixed deposits, depreciation can quietly erode your real returns. Let’s say your Indian mutual fund delivers 12% annualized growth in INR. Sounds great, right? Subtract a 4-9% rupee depreciation when converting back to your home currency, and your effective return in dollars or pounds drops sharply—sometimes to single digits or even flat. Over years, this compounds into a massive gap.

Take real estate, a favorite for NRIs. The falling rupee has made Indian properties feel like a sale for foreign buyers. A flat in Mumbai or Bangalore that once required converting dollars at a higher rate now feels more accessible. Yet, if you plan to sell and repatriate later, the same currency risk applies unless hedged. NRI real estate investments have seen renewed interest in 2026 precisely because of this “buy low” dynamic, but experts warn that without proper planning, exit strategies can sting.

Mutual funds and stocks follow a similar pattern. NRI mutual fund portfolios in index funds or sectoral plays often shine in rupee terms during India’s growth phases, but the forex drag turns them into underperformers on a global balance sheet. Add in taxes, repatriation rules under FEMA, and compliance, and the picture gets complex.

The FPI Angle: Why Outflows Are Accelerating and What It Means for Markets

Foreign Portfolio Investors (FPIs) face an even starker version of this reality. Their mandate is simple: deliver strong returns in dollar terms to global clients. When the rupee depreciates, even solid Indian corporate earnings get wiped out on conversion. This explains the record FPI outflow India in 2026—billions pulled from equities and even bonds as investors reallocate to safer or higher-yielding spots amid oil volatility and rupee weakness.

Brokerages like Bernstein highlighted these risks in reports, cutting Nifty targets and adopting a neutral stance. They pointed to potential GDP slowdowns, inflation spikes above 6%, and rupee pressures if oil stays elevated. FPIs aren’t fleeing India’s growth story entirely—many still believe in the long-term fundamentals—but short-term currency risk management has become non-negotiable. The result? Higher market volatility, wider bond yields, and opportunities for patient domestic investors.

The Big Debate: Blessing, Curse, or Something in Between?

Is the falling rupee purely destructive? Not quite. Multiple perspectives exist. For exporters, IT firms, and pharma companies earning in dollars, a weaker rupee boosts competitiveness—revenues translate into fatter rupee profits. Small and medium businesses in manufacturing have seen margins improve.

For NRIs with ongoing expenses in India (family support, property maintenance), depreciation acts as a natural hedge. Some analysts even call it a “buying window” for long-term NRI investment India plays, arguing that India’s structural growth will eventually outweigh currency noise.

On the flip side, importers, households facing higher fuel and grocery costs, and unhedged investors suffer. Chronic depreciation fuels inflation, raises borrowing costs, and can dent overall confidence. For FPIs, the math is unforgiving: currency losses have turned many India allocations into drags on global portfolios.

Balanced view? It depends on your horizon, risk appetite, and strategy. Short-term pain for unhedged portfolios; potential long-term gain for those who adapt.

Real Stories: Triumphs, Tumbles, and Lessons from the Diaspora

Let’s hear from those living it. Arjun, 29, in the US: He ignored currency signals and parked savings in Indian equities. “My portfolio grew 18% in rupees, but after conversion and the 2026 slide, I barely broke even. Lesson learned—never ignore forex.”

Contrast with Sneha, 38, in Singapore: She used a 12-month forward contract to lock rates on part of her portfolio and diversified into GIFT City opportunities. “The rupee dip let me buy more shares at lower effective prices, and my hedge protected the upside. Now my returns feel real.”

These aren’t isolated cases. Across Gulf NRIs and tech professionals abroad, 2026 has become a year of recalibration—some doubling down on India, others shifting to multi-currency assets.

Safe Strategies: Hedging and Tactics to Protect Your Wealth

Ready to safeguard your investments? Here’s how to navigate rupee depreciation 2026 smartly:

- Start with Hedging Basics: NRIs can access exchange-traded currency futures and options on Indian exchanges to lock in rates. Forward contracts let you fix today’s exchange rate for future repatriation—simple yet powerful insurance.

- Diversify Across Currencies and Assets: Don’t put everything in rupee-denominated investments. Explore GIFT City products, international mutual funds, or foreign currency fixed deposits that reduce pure INR exposure.

- Leverage Remittance Timing: Send money home during dips to maximize rupee value. Pair it with NRE accounts for tax-free interest and easy repatriation.

- Focus on Real Assets with Care: NRI real estate shines now, but choose liquid markets (Tier-1 cities) and factor in rental yields that can offset currency swings.

- Consult Pros and Track Macros: Work with a certified financial planner familiar with NRI rules. Monitor oil prices, RBI moves, and FPI trends 2026 closely.

- Natural Hedges: If you have India-based expenses or export-linked income, use them to offset risk without complex instruments.

Remember, hedging isn’t about speculation—it’s about peace of mind.

NRI and FPI Smart Moves: Investment Tactics for 2026

Beyond hedging, think tactically. For NRIs: Prioritize sectors resilient to oil shocks (IT, renewables, domestic consumption). Dollar-cost average into mutual funds during volatility. For FPIs: Look for companies with strong forex hedging on their books or those benefiting from rupee weakness.

A fresh angle? View the weak rupee as India’s way of signaling value. With proper currency risk management, 2026 could mark the start of stronger, more resilient portfolios rather than a year of regret.

Wrapping It Up: Your Move in the Rupee Storm

The falling rupee in 2026 isn’t black-and-white. For some NRIs and FPIs, it’s eroded profits and triggered outflows. For others who acted with insight, it created entry points and forced smarter habits. The difference lies in preparation: understanding the risks, embracing hedging strategies India, and staying informed.

If the rupee volatility has you rethinking your NRI investment India or FPI exposure, now’s the time to act. Start small—review your portfolio, speak to an advisor, and explore one hedging tool. India’s growth story remains compelling; the rupee just adds a layer of strategy.

What’s your experience with rupee depreciation 2026? Have you adjusted your investments, or are you riding it out? Drop your story in the comments below—let’s learn from each other and build smarter financial futures together. Your wealth deserves protection in every currency storm.

You May Like This

Advertisement

You May Like This

Advertisement

Advertisement

Advertisement