Advertisement

- Updated on April 17, 2026

- IST 4:26 am

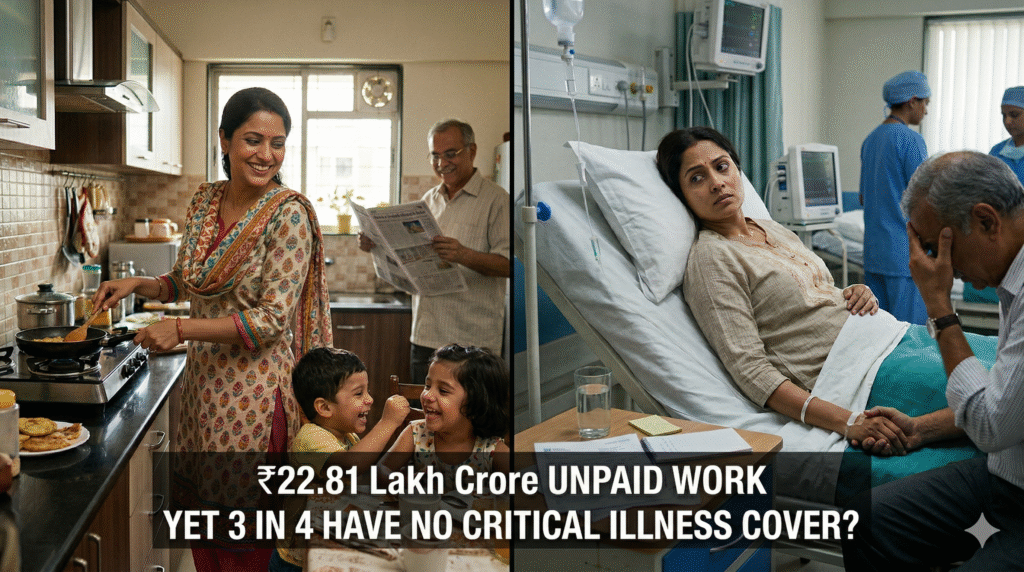

She Works for Free, But You Won’t Insure Her? The Shocking ₹22 Lakh Crore Insurance Gap!

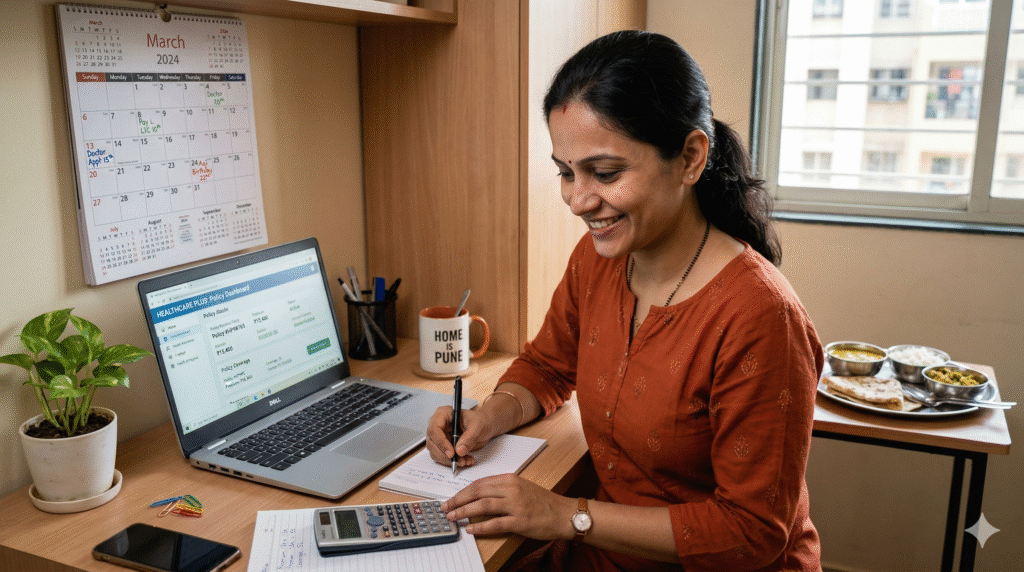

Imagine this: Rekha, a 42-year-old homemaker from Mumbai, wakes up at 5 AM every day. She packs tiffins for her husband and two school-going kids, manages the elderly in-laws’ medicines, handles grocery runs in the humid Mumbai traffic, and keeps the home spotless—all while juggling festival preparations and family finances. Her “job” never ends, yet she draws no salary. Then comes the diagnosis: stage-2 breast cancer. Treatments, chemotherapy sessions, special nutrition, and a helper for household chores add up to over ₹18 lakh in months. The family’s emergency savings vanish. Her husband takes loans at high interest. The kids’ coaching classes get cut. Rekha watches helplessly as her world unravels. “I always thought the family floater was enough. Who would insure me when I’m not earning?” she later tells her sister, voice breaking.

Now picture Meena, 37, from Hyderabad. She too runs her household like a silent CEO—cooking Andhra-style meals, helping her daughter with online classes, caring for her diabetic mother-in-law. But five years ago, her husband added a dedicated critical illness cover in her name. When Meena faced a sudden heart complication requiring surgery, the policy paid a lump-sum ₹25 lakh within weeks. It covered hospital bills beyond the basic policy, hired a full-time cook and maid, paid for recovery supplements, and even kept the family’s EMIs running smoothly. “It felt like a safety net I never knew I needed,” Meena shares with a relieved smile. “My role at home didn’t stop; the cover made sure the family didn’t break.”

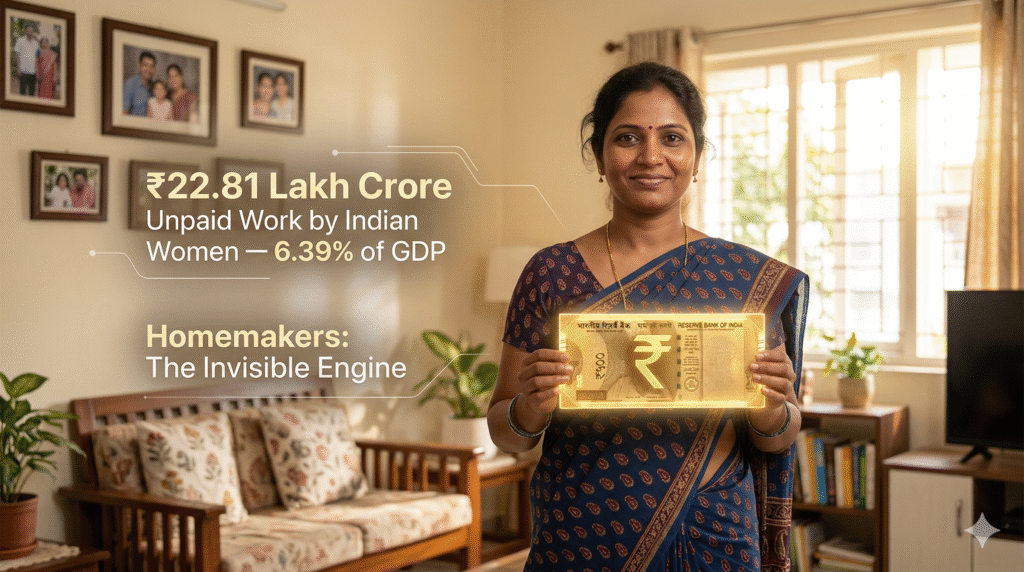

So, what separates these two real-life stories unfolding in thousands of Indian homes? The ₹22.81 lakh crore reality. Indian women contribute this staggering amount annually through unpaid household work—equivalent to nearly 6.39% of India’s GDP—yet a shocking 3 in 4 homemakers have zero critical illness cover. This isn’t just statistics; it’s a hidden financial time bomb for families. In this blog, we’ll unpack the true value of homemakers’ unpaid work, the massive protection gap in homemaker insurance, why one medical emergency can wipe out years of savings, and how smart critical illness cover for women can change everything. We’ll explore multiple perspectives, share practical desi tips, and give you actionable steps tailored for Indian families. Let’s bridge this women protection gap together—because the heart of your home deserves real financial protection.

The Unsung Economy: Valuing Homemakers’ Unpaid Work in India

Let’s start with the numbers that should make every family pause. Recent research from Bajaj Capital Insurance Broking’s “Shakti Shield 2026” report puts the economic value of Indian women’s unpaid household and care work at ₹22.81 lakh crore. That’s not pocket money—it powers the entire economy. Women spend an average of 7 hours daily on unpaid domestic tasks—cooking, cleaning, childcare, eldercare, fetching water or groceries—compared to men’s 1-2 hours. This “invisible engine” lets husbands focus on careers, kids excel in studies, and elders receive loving care.

Think of a homemaker as the unsung CEO of the family enterprise. She manages budgets, plans meals to keep everyone healthy, coordinates schedules, and provides emotional glue during tough times. Without her, the “business” (your home) would need expensive outsourcing—maids, cooks, nannies, drivers—easily costing ₹25,000–40,000 monthly in cities. Yet in personal finance conversations, she’s often labeled a “dependent.” This mindset fuels the critical illness cover women gap. Families insure the earning member but overlook the one whose absence creates chaos far beyond money.

From a critical thinking lens, multiple perspectives exist. Some argue unpaid work isn’t “productive” because it’s not monetized. Others see it as cultural duty. But research-driven views from time-use surveys show this labor keeps India’s GDP afloat indirectly. Ignoring it in insurance planning is like running a company without protecting its key operations manager. For Indian women aged 15-45—the prime homemaking and family-building years—this oversight is especially risky as lifestyle diseases rise.

What Is Critical Illness Cover? Timing, Lump Sum, and Real Relief

Unlike standard health insurance that reimburses hospital bills after claims, critical illness (CI) cover works differently—and that difference can save families. It pays a one-time lump-sum amount (typically ₹5 lakh to ₹50 lakh, depending on the plan) the moment a doctor diagnoses a covered critical illness. No bills needed. Use the money any way you want: advanced treatment, second opinions, home nursing, lost income replacement, or even keeping the kids’ education uninterrupted.

Common covered conditions include cancer (of all types), heart attack, stroke, kidney failure, major organ transplant, paralysis, and more—up to 30-40 illnesses in comprehensive plans. For homemakers, this lump sum is gold. When she can’t cook, clean, or care, the family doesn’t just lose emotional support; practical costs skyrocket. A maid plus cook might cost ₹15,000 monthly. Special diets and travel to super-specialty hospitals add thousands more. CI cover steps in exactly when regular policies fall short.

In India, with medical inflation running at 11.5-14% annually, treatment costs have exploded. Cancer therapy can easily hit ₹10-25 lakh over months. Heart procedures range from ₹2-10 lakh. Without dedicated homemaker insurance or CI rider, families dip into retirement savings or take high-interest loans—pushing many into debt traps. Experts recommend at least ₹20-50 lakh cover for homemakers based on family size and city.

The Big Protection Gap: Why 3 in 4 Homemakers Still Lack Cover

Here’s where it gets eye-opening. The same Bajaj Capital report reveals that 77% of homemakers—roughly 3 in 4—have no critical illness cover. Overall, nearly 29% of Indian women lack it, but the gap widens dramatically for non-working spouses. Over 45% of women still depend entirely on spousal or parental policies.

Why this persistent women financial security blind spot? Several reasons stand out:

- Myth of the Family Floater: Many assume “we’re all covered under husband’s policy.” But floaters share a single sum insured. One major claim can leave others exposed. CI riders, when present, often have lower limits or waiting periods.

- “She Doesn’t Earn, So Why Insure?” Mindset: Cultural views still see homemakers as low-risk. Yet health doesn’t discriminate by salary slip.

- Awareness and Priority Gap: Insurance awareness for women remains low. Families prioritize term life for earners but skip CI for the home manager.

- Perceived Cost: Premiums (₹3,000–15,000 yearly for ₹10-25 lakh cover, depending on age) feel like an extra burden in inflation-hit budgets.

This unpaid work value India reality clashes hard with the insurance reality. A single health shock—now more common with rising pollution, stress, and sedentary lifestyles among women—can derail an entire family’s dreams.

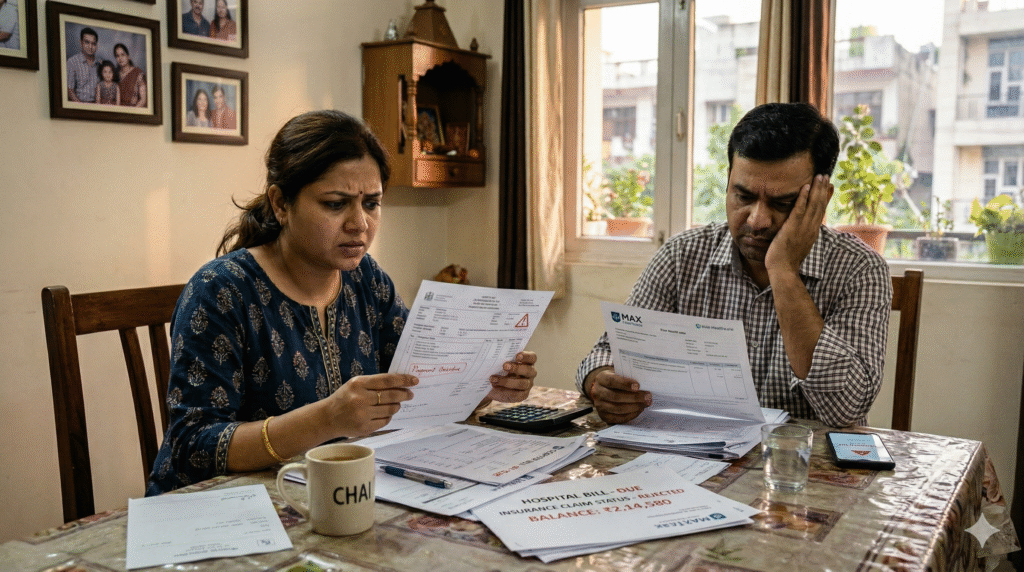

The Risks Without Cover: One Emergency Can Erase Everything

Skip critical illness cover for housewives and the fallout is swift and severe. Out-of-pocket expenses for critical illnesses devour savings. Families sell gold, delay marriages, or pull kids from good schools. Emotional toll follows: guilt for the homemaker, stress for the breadwinner, anxiety for children.

Balanced view: Not every family can afford multiple policies immediately. But ignoring the gap is riskier. Government schemes like Ayushman Bharat help the poorest, but middle-class “missing middle” families fall through cracks. Medical inflation outpaces general inflation, making delays costly. Cancer and cardiac cases among women under 45 are climbing. Without protection, the homemaker’s “free” work suddenly demands paid replacements—at market rates she once provided for free.

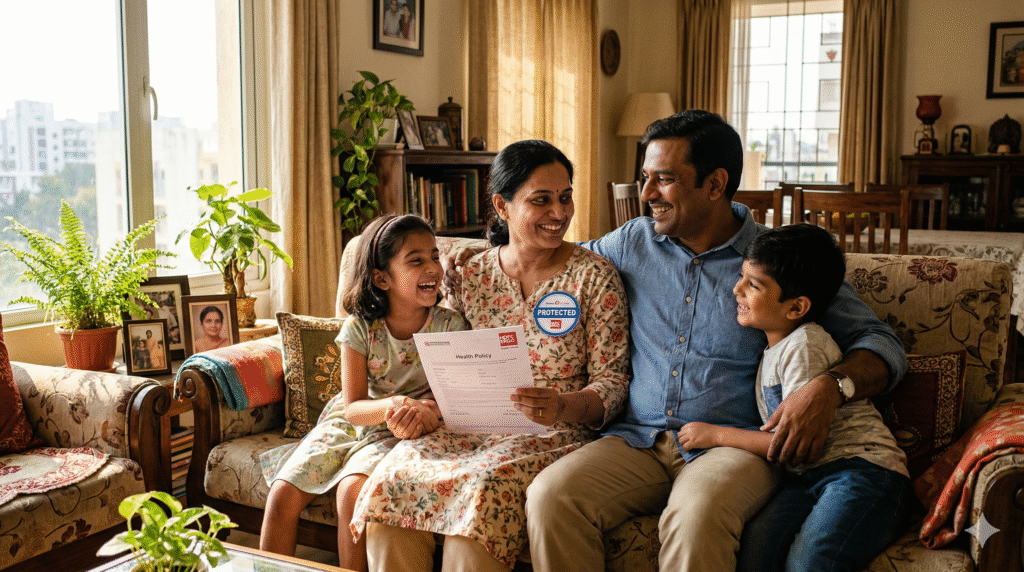

Why Critical Illness Cover for Homemakers Is a Smart Move: Benefits That Go Beyond Money

The upside is clear and compelling:

- Immediate Financial Buffer: Lump sum arrives fast—no endless paperwork.

- Lifestyle Continuity: Hire help so kids’ routines stay normal and husband focuses on work.

- Empowerment and Recognition: Buying homemaker insurance acknowledges her ₹22.81 lakh crore contribution.

- Tax Perks: Premiums qualify under Section 80D for deductions.

- Long-Term Family Security: Protects against debt traps and preserves wealth for education or retirement.

Experts note that families with proper CI cover recover faster emotionally and financially. It’s not just insurance—it’s peace of mind.

The Indian Twist: Tradition Meets Modern Risks

Fasting during Navratri, cooking lavish Diwali feasts, managing joint-family dynamics—Indian homemakers juggle cultural roles beautifully. But nuclear families, urban stress, junk food, and pollution have increased women-specific risks like breast cancer, PCOS complications, and heart issues. Traditional support systems (grandparents, relatives) are fading. This makes dedicated health insurance for housewives essential, not optional.

Many families now blend tradition with modernity—celebrating women’s financial independence while still undervaluing their insurance needs. Closing the insurance awareness women gap starts with open kitchen-table conversations.

Real Stories: Triumphs and Hard Lessons from Indian Homes

Meera, 40, from Pune, faced thyroid cancer without CI cover. “We managed somehow, but it took two years to recover financially,” she says. Her husband’s promotion dreams were delayed.

Riya, 34, from Chennai, had a CI plan. Her kidney-related issue was handled smoothly. “The payout let me rest and heal while a helper kept our home running. My family stayed strong,” she beams.

These aren’t isolated cases. Forums and advisors hear similar tales daily—proving one policy can turn crisis into manageable challenge.

Practical Tips: How to Get Critical Illness Cover Right for Homemakers

Thinking of acting? Here’s a step-by-step guide:

- Start the Conversation: Sit with your spouse and discuss her unpaid work value. Calculate replacement costs.

- Assess Coverage Needs: Review existing family floater. Add a standalone CI plan or rider for her.

- Choose Wisely: Look for 30+ illnesses covered, no-claim bonus, and high claim-settlement ratio insurers. Aim for ₹15-50 lakh sum based on city and family size.

- Compare Family Floater vs Individual: Floaters are convenient but shared. Individual CI gives dedicated lump sum—better for homemakers.

- Ease In Smartly: Buy early (lower premiums). Include women-specific conditions if available.

- Review Yearly: Update as kids grow or health changes.

- Consult Professionals: Talk to certified advisors. Use online tools but verify personally.

Desi Financial Hacks: Making Protection Affordable and Effective

Budget the premium like a monthly grocery item—₹300-1,000. Link it to festival savings or tax refunds. Teach kids about financial literacy early. Combine with preventive health (yoga, balanced diet) to lower risks and premiums. Apps make renewals effortless. View it as investing in her—and your family’s—future.

Wrapping It Up: To Insure or Risk It All?

The ₹22.81 lakh crore reality is clear: homemakers power Indian families yet remain among the most underinsured. 3 in 4 without critical illness cover is a gap we can no longer ignore. One diagnosis shouldn’t erase lifetimes of hard work and love.

If this hits home, take action today. Talk to your partner. Review your policies. Explore homemaker insurance and critical illness cover women options that fit your budget. PCOS, cancer cover India, or general health insurance for housewives—start small but start now.

What’s your take? Have you added CI cover for the homemaker in your life? Faced a health scare without it? Drop your story in the comments—we read every one and it helps spread awareness. Share this blog with friends and family. Together, let’s close the women protection gap and secure every Indian home.

Your family’s future thanks you.

You May Like This

Advertisement

You May Like This

Advertisement

Advertisement

Advertisement