Advertisement

- Updated on April 17, 2026

- IST 6:22 am

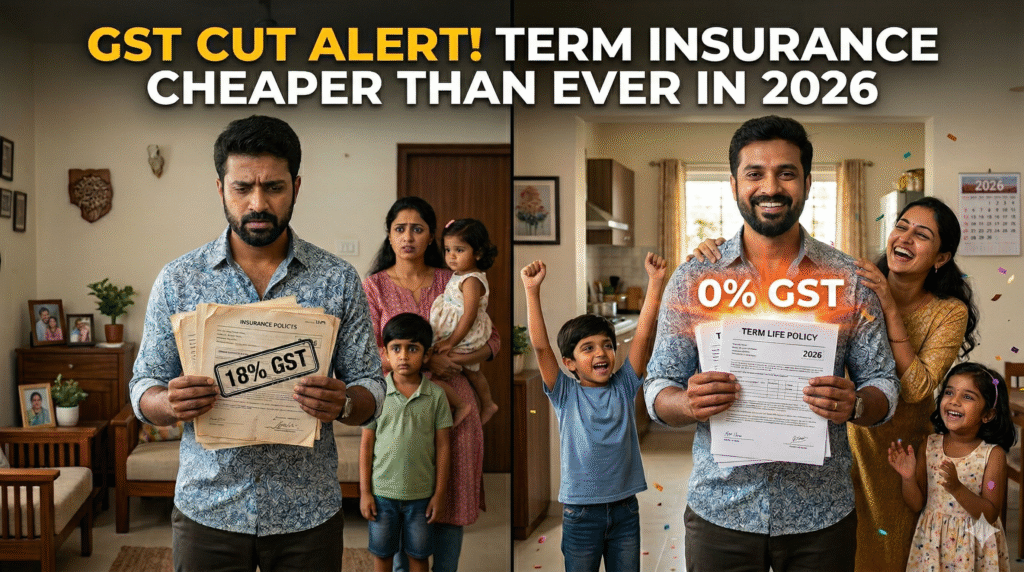

GST Rate Cut Alert! Why Term Insurance Premiums are at an All-Time Low in 2026 – Buy Now!

Imagine this: Arjun, a 32-year-old software engineer from Bangalore, bought his term plan in late 2024. He wanted ₹2 crore cover for his young family—wife and two kids. The base premium looked reasonable at around ₹18,000 a year, but after 18% GST, it jumped to over ₹21,240. He paid extra every year without realizing the change coming. Fast-forward to 2026: medical inflation hit, his company laid off a few colleagues, and suddenly he wished he had waited. “I could have saved thousands annually on the same cover,” he tells his wife one evening, scrolling through new quotes with regret.

Now picture Priya, 29, a marketing professional from Delhi. She and her husband were planning their first child when the GST reform hit in September 2025. With zero GST and fresh competition from the Insurance Amendment Bill, she locked in a ₹1.5 crore low-premium term plan for just ₹9,800 a year—pure base premium, no tax added. Six months later, she’s pregnant, her husband’s startup is growing, and the policy feels like a warm safety net. “It’s like the government and insurers finally teamed up to make protection affordable for people like us,” she shares excitedly with her friends in their WhatsApp group.

So, what’s the truth? Is 2026 really the cheapest year to buy term insurance in India, or is it just smart marketing? With the GST rate cut on individual life insurance from 18% to 0% and the Insurance Amendment Bill opening doors to 100% FDI, insurers are racing to offer better, cheaper products—projected 8–13% growth ahead. In this blog, we’ll unpack the massive savings on term insurance cheap 2026, how GST on insurance changes your premium outlay, the top 5 low-premium term plans for young buyers, real-life Indian stories, and smart tips to grab the best term plan India right now. Let’s dive in and secure your family’s future while the window is wide open!

Understanding Term Insurance: Pure Protection at Its Best

First, let’s get the basics right. Term insurance isn’t like those old endowment policies that mix insurance with investment and give low returns. It’s pure life cover—simple, powerful, and designed for one thing: to financially protect your loved ones if something happens to you during the policy term. No maturity benefits, no cash value, just a high sum assured at a fraction of the cost.

Think of it like a safety net under a tightrope. You walk the rope (live your life, pay EMIs, raise kids), and the net (the policy) catches your family if you fall. For young Indians aged 25–40—the prime earning and family-building years—this is the smartest financial tool. A 30-year-old non-smoker can get ₹1 crore cover for as low as ₹400–600 per month (now even lower with zero GST). That’s cheaper than many monthly subscriptions or coffee runs!

But here’s the twist most people miss: term insurance cheap 2026 isn’t just about low base rates anymore. The GST cut has wiped out the 18% tax that used to inflate every premium. Plus, the Insurance Amendment Bill passed in late 2025 allows full foreign ownership, bringing global tech, better underwriting, faster claims, and more competition. Insurers are now in overdrive to grab market share, meaning lower premiums and innovative features for young buyer insurance and insurance for millennials.

The Game-Changing Reforms: Zero GST + 100% FDI = Historic Opportunity

Here’s where 2026 becomes legendary for low premium term plan seekers. From September 22, 2025, the GST Council slashed GST on all individual life insurance policies—including term plans—from 18% to zero. Previously, a ₹15,000 base premium became ₹17,700 after tax. Now? You pay exactly ₹15,000. Over a 20–30 year policy, that’s tens of thousands saved—money that can fund your child’s education or your retirement.

On top of this, the Insurance Amendment Bill (Sabka Bima Sabki Raksha) raised FDI to 100% under the automatic route. Foreign giants are now eyeing India with fresh capital, advanced AI underwriting, digital issuance, and competitive pricing. Industry experts predict 8–13% annual growth as penetration rises from the current low levels. More players mean better options, quicker policy issuance, and yes—cheaper term insurance for family.

From a critical thinking lens, not everyone agrees it’s all sunshine. Some worry insurers might quietly raise base premiums to offset lost input tax credits. Others say the real benefit is long-term as competition intensifies. But the numbers don’t lie: for most young buyers, the net effect is a clear drop in out-of-pocket cost. This is the lowest life cover cost we’ve seen in years.

The Big Impact: How Much Can You Actually Save in 2026?

Let’s talk real money with a quick example. Take a healthy 28-year-old male in Mumbai buying ₹2 crore cover till age 65:

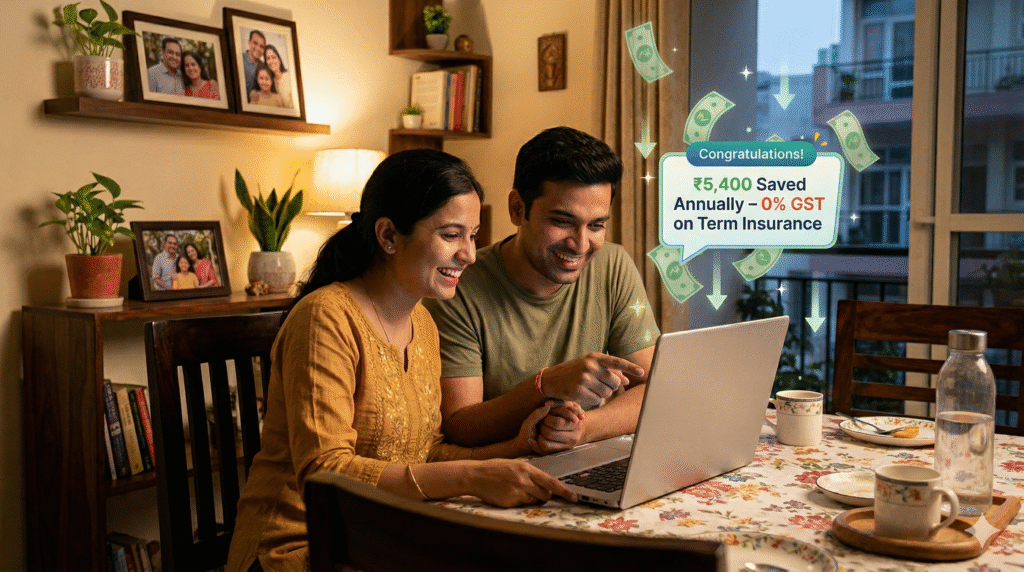

- Pre-2025 (with 18% GST): Base ~₹22,000 → Total ~₹25,960 per year.

- 2026 (zero GST + competitive rates): Base now ~₹19,500–₹21,000 → You save ₹4,000–₹6,000+ annually.

Over 30 years? That’s easily ₹1.2–1.8 lakh in direct savings. For women, premiums are often 20–30% lower due to better longevity stats. Add online term insurance discounts (up to 15–18% extra for direct buys), and the numbers become even sweeter.

Multiple perspectives exist. Traditionalists say “buy term and invest the rest” still holds. Tech-savvy millennials love the seamless apps and instant issuance. Financial advisors stress buying early—lock in low rates before age or health changes push premiums up.

Top 5 Cheapest Term Plans for 2026: Real Comparison for Young Buyers

Here are the standout low premium term plans making waves right now (illustrative premiums for a 30-year-old healthy non-smoker, ₹1 crore cover, regular pay, till age 65—always get personalized quotes):

- ICICI Pru iProtect Smart Plus: Often the cheapest entry point (~₹440–₹520/month). Excellent riders, high claim settlement.

- HDFC Life Click 2 Protect Supreme: Feature-rich with return of premium option, strong brand trust (~₹520–₹600/month).

- Tata AIA Sampoorna Raksha Promise: Flexible payout options, competitive rates (~₹501–₹580/month).

- Max Life Smart Term Plan Plus: Top claim settlement ratio, innovative increasing cover (~₹550–₹630/month).

- Bajaj Allianz eTouch II: Pure digital play, very affordable for tech users (~₹480–₹570/month).

These best term plan India options beat older policies hands-down thanks to zero GST on insurance and tech-driven efficiency. Always compare on claim settlement ratio (all above 98–99.7%), insurer solvency, and rider flexibility.

The Indian Twist: Protecting Desi Dreams in a Changing Economy

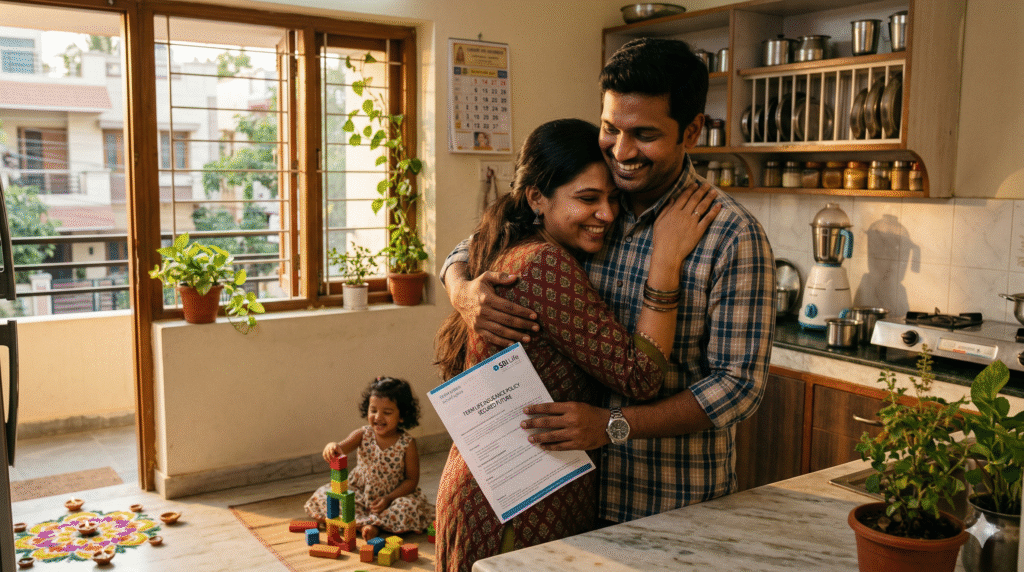

In India, we juggle joint families, rising EMIs, kids’ coaching fees, and elderly care—all on one or two incomes. Term insurance for family isn’t a luxury; it’s a necessity. The GST cut feels like Diwali bonus for millions of young couples in Gurugram, Hyderabad, or Pune. With nuclear families on the rise and traditional safety nets thinning, this reform bridges the protection gap perfectly.

Our love for gold and property is legendary, but they don’t pay hospital bills or school fees instantly. Term plans do—tax-free under Section 10(10D). Combine that with Section 80C/80D benefits on premiums, and it’s a no-brainer for personal finance family planning.

Real Stories: Triumphs and Missed Chances

Rahul from earlier? He’s now upgrading his old policy where possible and advising friends to buy fresh covers in 2026. “The savings are real,” he says.

On the bright side, Neha, 27, from Chennai, bought online last month: “I got ₹1.5 crore cover for less than my previous EMI on a two-wheeler. My parents finally sleep peacefully knowing the family is protected.”

These aren’t rare. Forums and advisors report a surge in young buyer insurance purchases post-reform.

Safe Buying Tips: How to Grab the Best Deal in 2026

Ready to act? Follow these steps:

- Calculate your need: 10–15 times annual income minimum.

- Buy early—premiums rise with age and health.

- Compare online: Use neutral platforms for term insurance comparison.

- Choose riders wisely: Critical illness, accidental death, waiver of premium.

- Go digital: Online term insurance often has lower costs and faster processing.

- Check claim settlement ratio and solvency—aim for 98%+ and 200%+.

- Review yearly: Life changes, so does your cover.

Desi Financial Hacks: Making Term Insurance Work for Your Budget

Treat the premium like a non-negotiable “family tax”—budget it with your grocery or fuel expense. Pay yearly for extra discounts. Link it to salary hike or bonus. Teach kids about insurance awareness early. Pair it with a simple mutual fund SIP for the “invest the rest” strategy. Use apps that remind you of renewals and offer loyalty bonuses.

Wrapping It Up: The Window Is Open – Don’t Miss 2026’s Golden Chance

GST Cut & Tech Boost has made 2026 the cheapest year to buy term insurance—zero GST, more competition, lower premiums, and smarter products. For young Indians building careers and families, this is the moment to act. One smart decision today can protect generations tomorrow.

If this resonates, don’t wait. Get quotes today, compare the top plans, and secure low premium term plan peace of mind. What’s stopping you? Have you bought term insurance yet? Share your experience in the comments—we read every one and it helps spread awareness. Tag a friend who needs this and let’s close the protection gap together.

Your family’s biggest gift might just be the cheapest policy of your lifetime.

You May Like This

Advertisement

You May Like This

Advertisement

Advertisement

Advertisement