Advertisement

- Updated on April 17, 2026

- IST 4:09 am

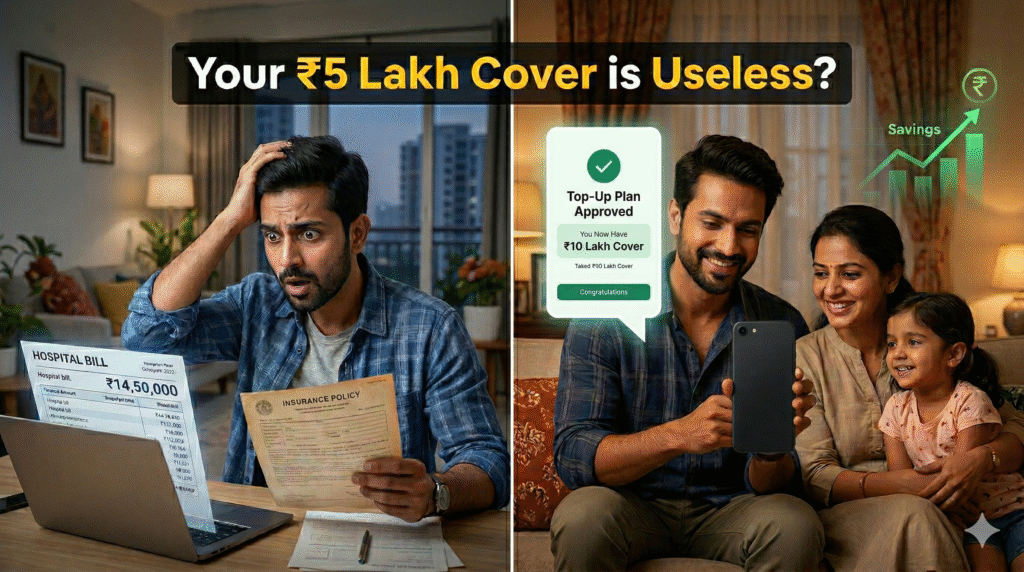

Imagine this: Amit, a 32-year-old IT manager from Gurugram, thought he had it all sorted. Five years ago, he bought a ₹5 lakh family floater for himself, his wife, and their toddler. “We’re young and healthy—why overpay?” he told his colleagues over coffee. Fast-forward to 2026: his wife needs a laparoscopic surgery for gallstones. The hospital bill? ₹9.8 lakh in a decent private facility in Delhi-NCR. His insurance covers only ₹5 lakh. The rest comes from his savings and a quick loan from his father. “I felt completely helpless,” Amit admits. “We were saving for a house, not medical emergencies.”

Now picture Priya, 28, a teacher from Pune. She faced the same reality check when her father’s knee replacement quote crossed ₹7 lakh. But instead of panicking, she sat down one weekend, ran the numbers on medical inflation, and added a super top-up plan. Today, her family’s total cover stands at ₹25 lakh effective cover—at almost the same premium cost. Her father got treated without dipping into retirement savings. “It was like discovering a hidden safety net,” she says with relief. “Why wait for a crisis?”

So, what’s the truth? Your ₹5 lakh health cover is useless! Medical inflation at 14% is bankrupting Indians in 2026—while general CPI hovers at just 5.4%. Your policy bought even three or four years ago has quietly lost more than half its real purchasing power. In this blog, we’ll unpack why this gap exists, how it’s silently eroding your family’s security, and—most importantly—a crystal-clear formula to calculate the right sum insured. We’ll share practical top-up strategies, desi-friendly tips, and real stories from young Indians like you. Let’s cut through the confusion and make sure your insurance actually protects you in today’s world.

Understanding Medical Inflation: The Silent Thief Stealing Your Peace of Mind

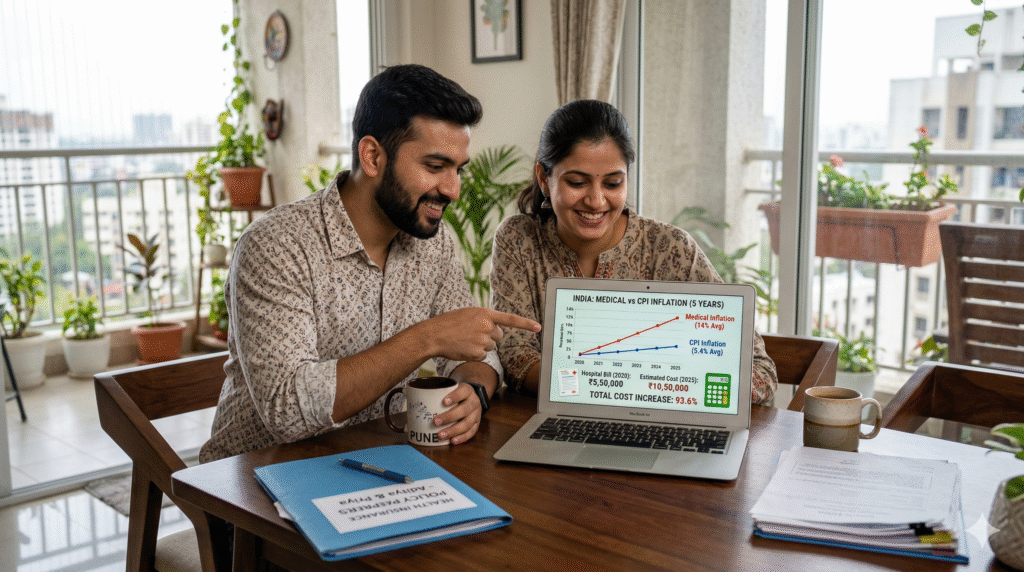

Medical inflation isn’t just another headline statistic—it’s a slow-burning fire that hits your wallet harder than regular price rises. While the Consumer Price Index (CPI) at 5.4% tracks everyday items like groceries and fuel, medical inflation in India is racing at 12-14% annually in private hospitals (as per 2026 industry projections). Why the massive difference? Think of it like two different worlds colliding.

Hospitals are upgrading to robotic surgery systems, importing expensive stents and cancer drugs, and paying top salaries to specialists who train abroad. Real estate costs for super-speciality facilities in metros like Mumbai, Bengaluru, and Hyderabad have skyrocketed. Add post-pandemic supply chain issues, higher doctor insurance premiums, and advanced diagnostics like PET-CT scans, and suddenly a simple hospital stay that cost ₹2 lakh in 2021 now easily touches ₹4-5 lakh.

For Indians aged 15-45—the millennials and Gen-Z building careers and starting families—this gap is especially dangerous. You’re not retired yet, but you’re also not immune to accidents, pregnancies with complications, or sudden critical illnesses. A ₹5 lakh policy that felt generous five years ago now barely covers a week in ICU in a Tier-1 city, where daily charges hover between ₹15,000 and ₹40,000.

How Inflation Quietly Makes Your Old Policy Worthless: The Math No One Tells You

Let’s make this real with simple numbers anyone can follow. Suppose you bought a ₹5 lakh health policy in 2021. At 14% compound medical inflation:

- After 1 year: effective value drops to roughly ₹4.39 lakh

- After 3 years: around ₹3.38 lakh

- After 5 years: barely ₹2.60 lakh in today’s hospital pricing power

That means your “₹5 lakh cover” today buys you only about half the treatment it once could. Hospitals don’t care about your policy date—they charge current rates. This is why thousands of families every year face the shock of “cashless” turning into huge out-of-pocket expenses.

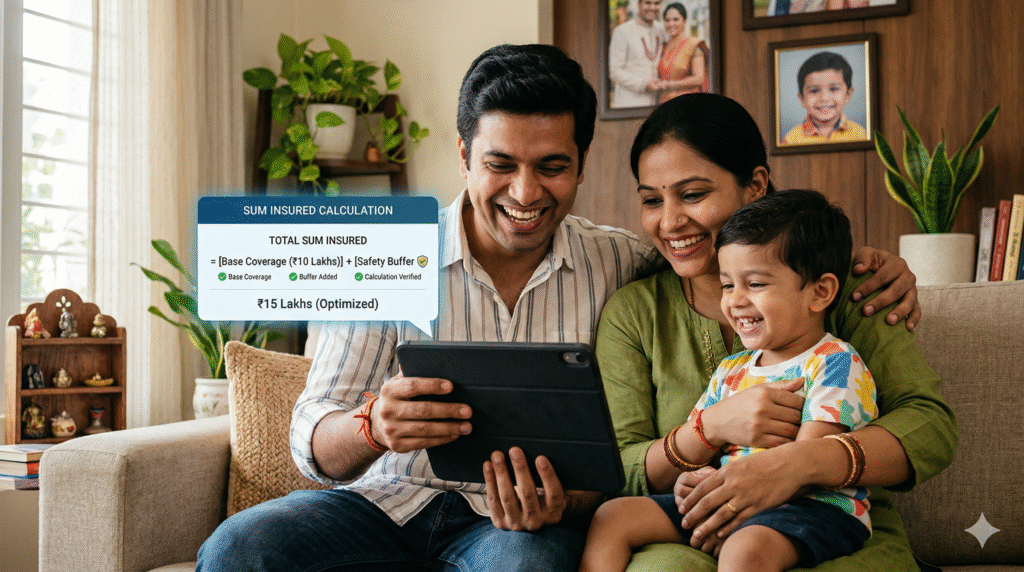

The formula to calculate your required sum insured is straightforward yet powerful:

Required Sum Insured = Current Estimated Treatment Cost × (1 + Medical Inflation Rate)^Number of Years

Or, more practically for families: Take your highest expected single-year medical expense (say ₹15-25 lakh for major illness) and multiply by 1.5-2x safety margin, then adjust upward every year by 10-14%. Young professionals should aim for at least ₹10-25 lakh base cover plus a super top-up of ₹20-50 lakh, depending on family size and city.

The Big Debate: Is 14% Medical Inflation Just Hype or a Real Threat?

Experts and policyholders land on different sides of this seesaw. Insurers and IRDAI reports acknowledge the rise but point to newer policies with inflation-adjusted features and group covers that help control costs. Some argue that government schemes like Ayushman Bharat and generic medicines are slowing the overall burden.

On the other side, consumer forums and hospital billing data tell a different story. Private healthcare (where most insured Indians go) has seen procedure costs jump 50-100% in five years for everything from deliveries to heart surgeries. Critical illness cases that once cost ₹8 lakh now demand ₹18-25 lakh with modern targeted therapies. The balanced truth? Medical inflation is very real and outpacing general CPI because healthcare isn’t a regular commodity—it’s driven by technology, regulation, and demand from an aging yet increasingly health-conscious population.

For the 15-45 age group juggling EMIs, school fees, and dreams of travel, ignoring this gap is like driving without a seatbelt—risky and potentially life-changing in the wrong way.

The Indian Twist: Private Hospitals, Family Duties, and Urban Realities

Fasting during festivals is a tradition we all know, but quietly paying medical bills isn’t. In India, we love our private hospitals for quick service and advanced care, yet that choice comes with a price tag that general inflation can’t explain. A normal delivery in a good Mumbai or Delhi hospital that cost ₹1.2 lakh in 2020 now easily crosses ₹2.8-4 lakh. Knee replacements? From ₹3 lakh to ₹6-8 lakh. Cancer treatment packages have doubled in many cases.

Our joint-family support system helps emotionally, but financially it often means dipping into retirement savings or taking loans. Young couples in Gurugram, Bengaluru, or Chennai are especially vulnerable—they’re the sandwich generation: caring for aging parents while raising kids. Traffic, work stress, and irregular meals add to lifestyle diseases that land us in hospital earlier than previous generations.

The good news? IRDAI has pushed for better portability and top-up products that let you scale protection without starting from scratch.

Real Stories: When Inflation Hit Home for Young Indians

Let’s hear from people just like you. Rahul, 29, from Hyderabad, had a ₹7 lakh family floater. When his mother needed angiography and stent in 2026, the bill was ₹14 lakh. Insurance paid ₹7 lakh; the rest wiped out his emergency fund. “I wish I had added a top-up earlier,” he says.

Contrast with Sneha, 26, from Kolkata: She reviewed her policy annually, increased her sum insured by 12% each year, and layered a low-cost super top-up. When her husband had an accident requiring surgery, the entire ₹11 lakh was covered seamlessly. “It gave us peace during the scariest time,” she shares.

These stories from metros and Tier-2 cities show one clear pattern: those who treat insurance as a “set it and forget it” product lose big; those who adjust for inflation win.

Calculating the Right Cover: Your Step-by-Step Safety Formula

Ready to check if your policy is dangerously low? Here’s exactly how:

- List your family’s current highest-risk scenarios (cancer, heart surgery, major accident, delivery complications).

- Get today’s average cost from hospital websites or your city’s pricing.

- Apply the inflation formula for the next 5-10 years.

- Add a 50-100% buffer for multiple claims or prolonged treatment.

- Consider city tier—Delhi/Mumbai costs 30-50% higher than smaller cities.

- Factor in co-pay, room rent caps, and waiting periods.

Pro tip: Use free online calculators from insurers or IRDAI-linked portals, then verify with a trusted advisor.

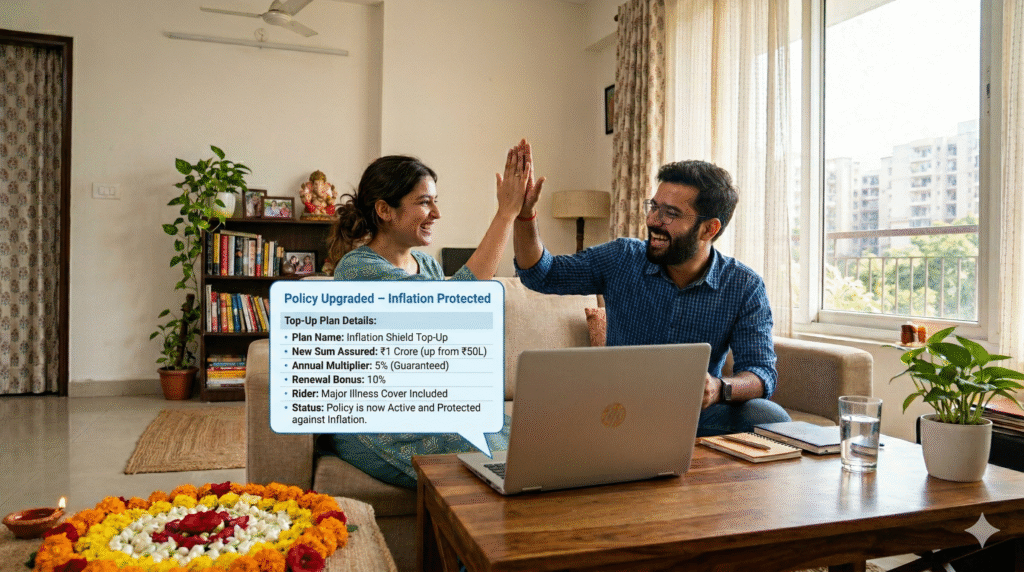

Top-Up Health Plans: The Smart Indian Fix for Inflation

Super top-up plans are the game-changer most young Indians overlook. They kick in only after a deductible (say ₹5 or 10 lakh), offering ₹20-50 lakh extra cover at a fraction of the premium of a full base policy. For a 30-year-old family, a ₹10 lakh base + ₹40 lakh super top-up often costs less than doubling the base policy while giving massive protection.

They’re flexible, portable, and perfect for inflation because you can renew and increase them easily. Combine with your existing policy—no need to cancel anything.

Desi Hacks to Beat Medical Inflation and Protect Your Savings

Here’s how to stay ahead without stress:

- Review and increase sum insured every year by at least 10-12%.

- Buy early—premiums and waiting periods are lower when you’re young.

- Opt for family floater + individual top-ups for critical illnesses.

- Maintain a healthy lifestyle (yoga, balanced diet, regular check-ups) to qualify for no-claim bonuses and lower loading.

- Choose policies with restoration of sum insured and no room rent capping.

- Use tax benefits under 80D wisely to offset costs.

- Build a separate medical emergency fund alongside insurance—aim for 3-6 months of expenses.

Small consistent actions today prevent huge financial shocks tomorrow.

Wrapping It Up: Don’t Let Inflation Make Your Cover Useless

14% medical inflation versus 5.4% CPI isn’t just numbers on a chart—it’s the difference between a manageable hospital bill and a family financial crisis. Your ₹5 lakh policy from a few years back is losing power fast, but you have the tools to fight back. Calculate your true need, layer smart top-ups, review annually, and treat protection as seriously as you treat your career or home loan.

If this blog made you reach for your policy documents, great! Take five minutes right now—check your sum insured, run the formula, and consider a top-up. Your future self (and your family) will thank you. What’s your experience with rising hospital costs? Did medical inflation surprise you too? Drop your story in the comments below—let’s learn from each other and build a more financially secure India, one smart policy at a time. Protect what matters most. Start today!

You May Like This

Advertisement

You May Like This

Advertisement

Advertisement

Advertisement