Advertisement

- Updated on April 17, 2026

- IST 2:19 am

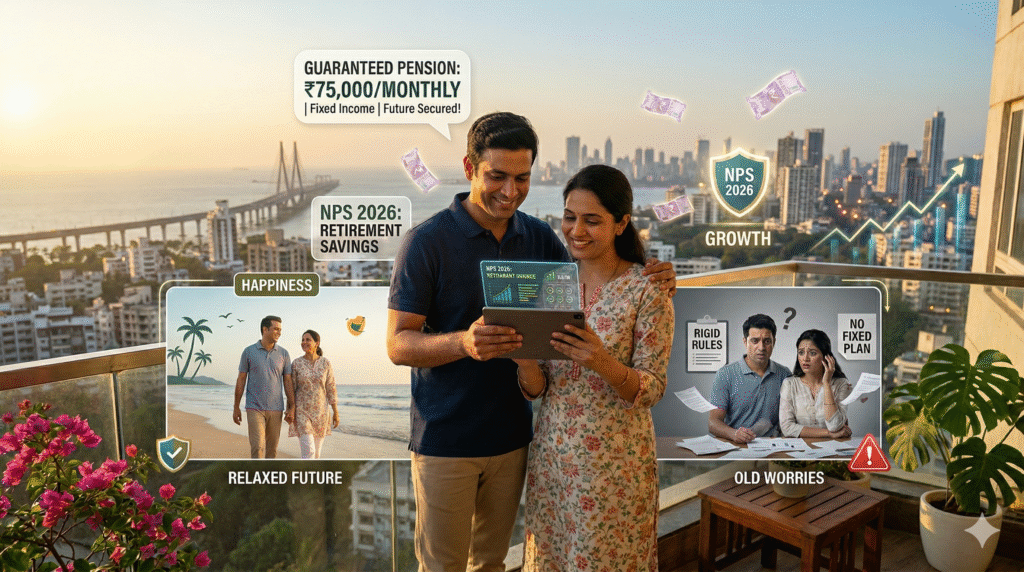

Imagine this: Rajesh, a 42-year-old IT manager from Pune, had been faithfully contributing to the National Pension System (NPS) since his late twenties. Years of market ups and downs, salary hikes, and family responsibilities later, he hit 60. Under the old rules, 40% of his hard-earned corpus was mandatorily locked into an annuity. His “fixed monthly income” felt more like a compromise—steady but modest, with inflation quietly chipping away at its real value. Emergency needs? Tough luck. He vented to his college group chat, “I saved for retirement, not to feel trapped by the rules!”

Now, picture Priya, 38, a marketing executive in Delhi who started her NPS journey early and timed it perfectly with the 2026 changes. At superannuation, she could withdraw up to 80% as a lump sum, use just 20% for a tailored annuity that guarantees her a fixed monthly pension for life, and invest the rest smartly through systematic options. Six months in, she’s drawing a comfortable ₹45,000 every month while her family enjoys financial breathing room. “The new rules didn’t just change NPS—they changed my retirement story,” she tells her friends over chai.

So, what’s the truth? Is India’s NPS revolution—with its game-changing “annuity escape” and PFRDA’s fresh rules—finally the key to a reliable fixed monthly income pension for ordinary Indians? With retirement planning India becoming a hot topic amid rising life expectancy and uncertain job markets, these updates are turning NPS into a more flexible, powerful tool. In this blog, we’ll unpack the new NPS changes 2026, the fixed monthly income pension mechanics, tax benefits NPS offers, how it stacks up against PPF and mutual funds, and practical steps to build your bulletproof retirement corpus. Whether you’re 25 and just starting or 45 and accelerating, let’s figure this out together—desi style.

Understanding NPS: Your Ticket to a Secure Retirement

First, let’s get the basics straight. The National Pension System isn’t some dusty government scheme—it’s a market-linked, voluntary retirement savings plan regulated by the Pension Fund Regulatory and Development Authority (PFRDA). Launched in 2004 and opened to all citizens in 2009, NPS lets you invest in equity, debt, government securities, or a mix, aiming for higher long-term returns than traditional fixed deposits or even PPF.

Think of it like a disciplined marathon: you contribute regularly (minimum ₹500 per month or ₹1,000 lump sum), your money grows through professional fund managers, and at retirement (age 60 or later), you create a retirement corpus that can deliver lifelong income. Unlike EPF (tied to your job) or PPF (15-year lock-in with fixed 7.1% returns), NPS gives you asset allocation control and the power of compounding over decades.

For young Indians aged 15-45—the salaried millennials, gig workers, and first-time investors—this is huge. Life expectancy is now pushing 70+, healthcare costs are soaring, and joint family support is shrinking. NPS steps in as your personal pension plan, blending growth potential with the promise of fixed monthly income via annuity. But until recently, the rigid 40% annuity rule turned many away. That changed dramatically in late 2025–early 2026.

NPS Changes 2026 Explained: The Annuity Escape and Fixed Monthly Income Revolution

Here’s where it gets exciting—the PFRDA’s 2025 amendments (effective 2026) have rewritten the exit playbook for non-government subscribers (All Citizen Model and Corporate NPS). The headline? Mandatory annuity purchase slashed from 40% to just 20% of your corpus. That means up to 80% can now come out as a lump sum, giving you real control to shape your fixed monthly income pension.

The new slabs make it even more practical:

- Corpus ≤ ₹8 lakh: 100% lump sum withdrawal—no annuity needed. Perfect for smaller savers who want full flexibility.

- ₹8–12 lakh: Up to ₹6 lakh as lump sum; balance via Systematic Unit Redemption (SUR) or annuity for at least 6 years.

- > ₹12 lakh: Up to 80% lump sum + minimum 20% into annuity for lifelong fixed payouts.

You can also opt for structured withdrawals (SUR or Systematic Lump Sum Withdrawal) instead of a one-time lump sum—ideal for creating your own “pension” stream without fully committing to traditional annuities. NPS Vatsalya, the scheme for minors, mirrors these flexible exit rules when the child turns 18, making it a smart gifting tool for parents.

The pitch? These rules deliver the best of both worlds: market-linked growth during your working years and the security of guaranteed monthly income later. Annuities from approved providers now cover just the minimum slice, leaving you free to invest the bulk elsewhere or use systematic plans for steady cash flow. It’s like finally being handed the steering wheel after years in the passenger seat.

The Big Debate: Pros and Cons of the New NPS Rules

Experts and everyday investors don’t fully agree—let’s break it down fairly.

The Pros: Why the 2026 Changes Could Make You Retirement-Rich

- Greater Flexibility and Control: The “annuity escape” lets you avoid over-committing to low-yield annuities. Take more as lump sum and create customized income streams via mutual fund SWPs or fixed-income options.

- Higher Potential Corpus: With 100% equity option now fully available and longer deferral possible, aggressive young investors can build bigger pots that translate into larger fixed monthly pensions.

- Tax Benefits NPS Shine: Contributions qualify for ₹1.5 lakh under 80C plus extra ₹50,000 under 80CCD(1B). Up to 60% lump sum withdrawal remains tax-free; annuity purchase is also tax-efficient at entry.

- Inflation-Beating Income: Annuity payouts can be structured for lifelong fixed income, with options for joint annuities (spouse protection) or increasing variants.

Priya’s story shows it: her optimized mix delivers ₹45,000 monthly while keeping liquidity for travel and medical needs.

The Cons: Where Caution Is Still Needed

- Market Risk Remains: Equity-heavy NPS can swing wildly—your corpus isn’t guaranteed like PPF.

- Annuity Taxation: While the purchase is tax-free, monthly pension payouts are taxable as income.

- Long Lock-In: Early exits still carry penalties; it’s designed for true long-term retirement planning India.

- Complexity for Beginners: Choosing asset allocation, annuity providers, and withdrawal options can feel overwhelming without guidance.

Rajesh’s frustration was real under old rules; the new ones reduce that pain but don’t eliminate the need for smart planning.

The Indian Twist: NPS Meets Desi Retirement Dreams

Retirement in India isn’t just about numbers—it’s about family weddings, medical emergencies, grandchildren’s education, and that dream Bharat trip. Traditional desi saving (gold, fixed deposits, PPF) often falls short on growth or liquidity. NPS 2026 changes bridge that gap beautifully.

Our culture values security and legacy. The reduced annuity mandate respects that by letting you keep more corpus for family needs while still securing a fixed monthly income pension. Combine NPS with PPF for the ultra-safe slice and mutual funds for growth—classic Indian portfolio diversification. For parents, NPS Vatsalya turns gifting into a lifelong pension gift for kids.

Real-life desi twist: Many in their 30s juggle EMIs, kids’ school fees, and elderly parents. Starting NPS early (even ₹2,000–5,000 monthly) leverages compounding so the 2026 flexibility delivers meaningful fixed income later—without sacrificing today’s lifestyle.

Real Stories: Triumphs and Tumbles from Indian Investors

Let’s hear from folks who’ve lived it.

- Vikram, 45, Mumbai: Switched aggressively to equity in 2020. Under new rules, he’ll withdraw 80% lump sum at 60 and use SUR for ₹60,000+ monthly income. “It feels like my money is finally working for me, not the other way around.”

- Meena, 32, Hyderabad: Started NPS Vatsalya for her 8-year-old daughter. The flexible 18-year exit options give her peace of mind. “It’s not just savings—it’s her future fixed income pension in the making.”

- Sandeep, 50, Chennai: Stuck with old rules earlier and regretted the high annuity lock-in. Now advising friends: “Don’t wait—the 2026 changes are your second chance.”

These stories prove NPS isn’t a one-size-fits-all magic wand. It’s a tool—how you use the new rules matters.

How to Build Your Bulletproof Retirement with NPS: Practical Tips

Ready to ride the NPS revolution? Here’s your step-by-step guide:

- Start Early and Stay Consistent: Open an NPS Tier-I account today. Even small SIPs compound massively by 60.

- Choose Smart Asset Allocation: Young (15-35)? Go 75% equity. Mid-40s? Shift gradually to debt for stability.

- Maximize Tax Benefits NPS: Claim full 80C + 80CCD(1B) deductions under old regime.

- Plan Your Exit Strategy Now: Model different corpus scenarios using online retirement corpus calculators. Decide lump sum vs annuity mix.

- Diversify Smartly: Pair NPS with PPF for safety and equity MFs for growth.

- Review Annually: Rebalance, check fund performance, and consult a SEBI-registered advisor.

- Involve Family: Discuss joint annuities and legacy planning early.

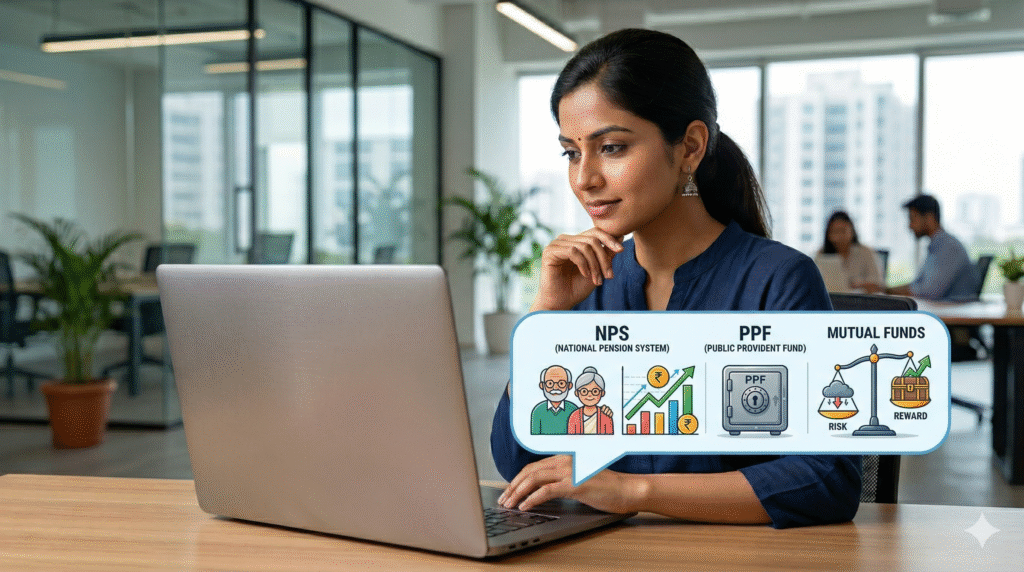

NPS vs PPF vs Mutual Funds: Quick Comparison for 2026

- Returns: NPS 8-12% (market-linked), PPF ~7.1% (guaranteed), MFs 10-15%+ (higher risk).

- Liquidity: NPS now far more flexible; PPF has partial withdrawals; MFs highly liquid.

- Tax: NPS offers extra ₹50k deduction; PPF is fully EEE; MFs have LTCG tax.

- Fixed Income Angle: NPS annuity wins for lifelong pension; PPF gives steady but smaller payouts.

For most 15-45 readers chasing guaranteed pension scheme vibes with growth, a 50-60% NPS allocation hits the sweet spot.

Wrapping It Up: Your Fixed Monthly Pension Awaits

The NPS changes 2026 aren’t just regulatory tweaks—they’re a revolution giving millions of Indians greater control over their fixed monthly income pension. The reduced annuity mandate, “annuity escape” for smaller corpuses, SUR flexibility, and strong tax benefits NPS make it one of the smartest retirement planning India tools right now.

It’s not about getting rich quick. It’s about building dignity and freedom in your golden years—whether that means stress-free travel, supporting family, or simply sleeping peacefully knowing bills are covered. The difference between worry and wealth? Starting today.

If the idea of a reliable fixed monthly pension excites you, open that NPS account this week. What’s your take? Already in NPS or planning to join the revolution? Drop your questions, corpus goals, or success stories in the comments below—let’s swap notes and build better retirements together!

You May Like This

Advertisement

You May Like This

Advertisement

Advertisement

Advertisement