Advertisement

- Updated on April 17, 2026

- IST 3:57 am

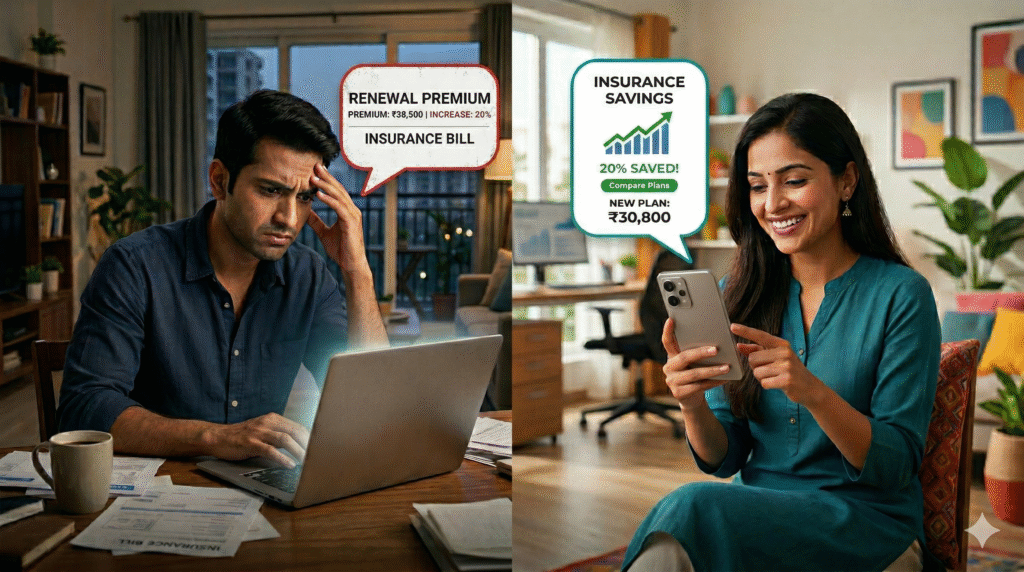

Imagine this: Rahul, a 34-year-old software engineer from Gurugram, opens his email one morning and freezes. His health insurance renewal notice stares back at him—premium up 22% from last year. “Did the company just hike it because they could?” he wonders, heart racing. He’s been loyal for five years, paid every instalment on time, and never claimed a rupee. Yet here he is, staring at an extra ₹8,000 a year for the same ₹10 lakh cover. Frustrated, he vents to his wife over chai: “Insurance was supposed to protect us, not drain us!”

Now picture Priya, 29, a marketing executive in Bengaluru. Same renewal shock hit her term life plan too. But instead of accepting it, she spent one evening comparing quotes online. She switched insurers, tweaked her sum assured slightly, and locked in a better plan. Result? She saved ₹12,500 annually while actually increasing her cover to ₹1 crore. “It felt like finding money in my old jeans,” she laughs. “Why didn’t I check earlier?”

So, what’s the truth? Your insurance just got 20% costlier in FY26—are you paying too much? The Indian insurance industry has hit a historic milestone with premium growth crossing 20% in key segments for the first time in recent years, driven by rising awareness, regulatory tweaks, and economic momentum. But for everyday families like yours, that “growth” often translates to steeper bills. In this blog, we’ll unpack why premiums surged, whether your hike is justified, and—most importantly—a simple, step-by-step guide to check if you’re overpaying. We’ll share desi-friendly tips, real stories from Indian policyholders, and smart ways to compare term and health insurance plans so you get the best rate without compromising protection. Let’s cut through the jargon and take control together!

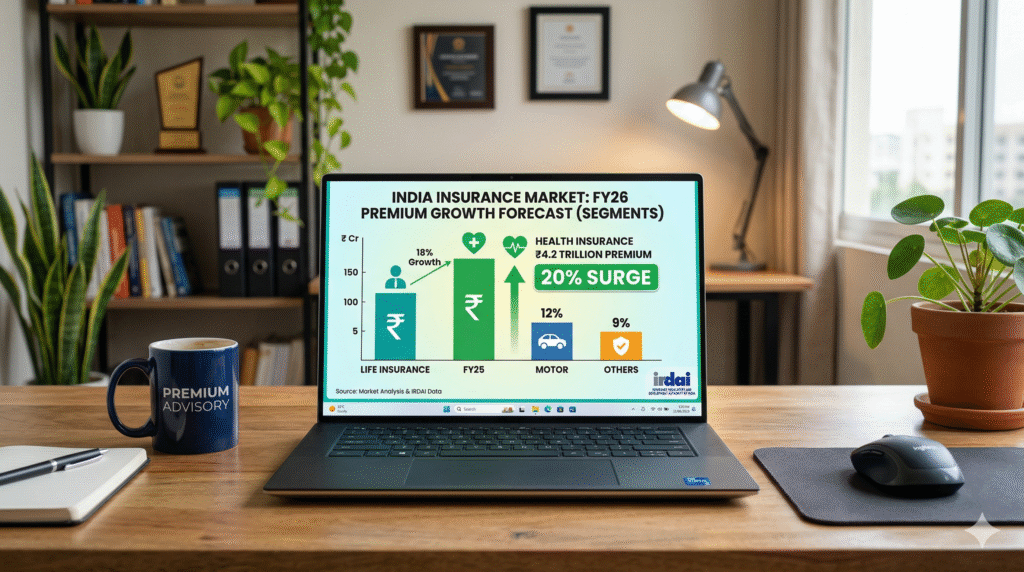

The FY26 Insurance Boom: What the 20% Surge Really Means

India’s insurance sector is on fire. According to recent IRDAI data and industry reports, overall premium income has seen double-digit growth, with certain non-life and health segments touching or exceeding 20% year-on-year in early FY26 months. Life insurance continues its steady climb, while health insurance—now the largest chunk of non-life—grew robustly thanks to greater awareness post-pandemic and schemes covering more lives.

But here’s the twist most headlines miss: industry growth doesn’t always mean better deals for you. Medical inflation is hovering around 11-14% annually. Hospitals charge more for everything from MRIs to cancer treatments. Insurers face higher claims, especially as waiting periods for pre-existing diseases shrink under new IRDAI rules. Add regulatory changes—like GST rationalisation on some health policies—and you get a perfect storm where companies pass on costs through higher premiums.

For young Indians aged 15-45 (many of you reading this), this hits hard. You’re building careers, starting families, and buying first homes. Insurance is no longer a “later” thing—it’s your safety net. Yet low insurance penetration in India (still under 5% of GDP in some metrics) means many are under-insured or overpaying on outdated plans. The good news? You don’t have to accept the first renewal quote. With tools and a bit of know-how, you can fight back.

Decoding Insurance Premiums: Term Life vs Health Plans in 2026

Let’s break it down simply, like chatting over filter coffee. Term insurance is pure protection—cheap, straightforward life cover that pays your family a lump sum if something happens to you. No fancy returns, just peace of mind. Premiums depend on age, health, lifestyle (smoking? family history?), and sum assured. In FY26, term insurance costs have stayed competitive thanks to more players entering the market and digital underwriting.

Health insurance, on the other hand, covers hospital bills, day-care procedures, and sometimes even OPD. Premiums here are surging faster because healthcare costs are skyrocketing. A simple appendix surgery that cost ₹50,000 a few years ago can now touch ₹1.5 lakh in a good city hospital. Insurers price based on age slabs, city tier, pre-existing conditions, and claim history.

Think of premiums like a seesaw: one side is your risk profile and medical inflation; the other is competition and IRDAI guidelines pushing transparency. When the seesaw tilts (as it did in FY26), your bill goes up—unless you actively balance it by shopping around.

The Big Debate: Are These Hikes Justified or Just Profit-Driven?

Experts and policyholders don’t see eye to eye—and that’s okay. Insurers argue hikes are necessary. Claims ratios have climbed; hospitals negotiate aggressively; newer regulations (shorter moratorium periods, inclusion of more conditions) raise their risk. IRDAI data shows health premiums underwritten crossed ₹1.17 lakh crore in recent years with steady growth.

On the flip side, many consumers feel blindsided. Stories of 20-30%+ renewal jumps for no-claim policyholders are common. One Bengaluru professional saw her family floater jump nearly 70% despite zero claims. Is it fair? Balanced view: some increase reflects real costs (medical inflation outpacing general inflation), but others stem from poor risk pooling or lack of competition awareness. Critical thinking here matters—blind loyalty costs money; informed switching saves it.

The Indian Twist: IRDAI Guidelines, Tax Benefits, and Desi Realities

Fasting isn’t new to Indians, and neither is insurance—think of it as modern “protection” like our grandparents’ fixed deposits. But unlike fixed deposits, insurance rules keep evolving. IRDAI’s latest guidelines emphasise fair pricing, claim settlement ratios above 99% for top players, and caps on senior citizen hikes (max 10% without approval). They’ve also pushed for better transparency—no more hidden clauses in fine print.

For the 15-45 age group, tax savings under Section 80C (term life) and 80D (health) make premiums even more attractive. A good plan can slash your taxable income while guarding against ₹20-50 lakh hospital bills. Yet many urban millennials still treat renewal as “autopay and forget.” Traffic, family duties, and work leave little time to dig deeper—that’s where the Indian twist bites.

Real Stories: Triumphs, Tumbles, and Lessons from 2026

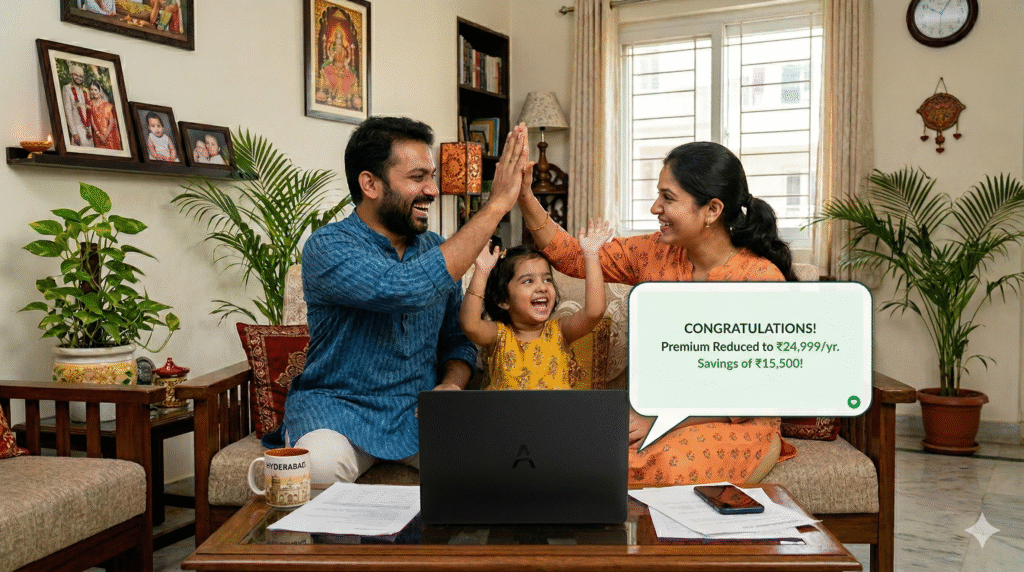

Let’s hear from folks just like you. Meera, 31, from Hyderabad, stuck with her old health plan and paid 25% more on renewal. Her doc later suggested a better option with same cover at lower cost. “I lost ₹15,000 because I didn’t compare,” she admits.

Contrast with Arjun, 27, Delhi: He used a comparison portal, added a super top-up, and cut his term premium by 18% while boosting cover. “My parents sleep better knowing the family is protected without breaking the bank,” he shares.

These aren’t exceptions. Across metros and Tier-2 cities, policyholders who treat insurance like a one-time purchase end up overpaying; those who review annually win.

Safe Steps: How to Check If You’re Overpaying – A Practical Guide

Ready to audit your policy? Follow these steps—no fancy degree needed:

- Gather Documents: Pull out your current policy schedule, last renewal notice, and claim history.

- Log into IRDAI Portal or Insurer App: Check your policy status and any approved rate changes.

- Use Free Comparison Tools: Head to trusted sites like Policybazaar or insurer websites. Enter age, city, sum assured, and health details for instant quotes.

- Calculate True Cost: Factor in GST (now rationalised on some plans), no-claim bonus discounts, and loading charges.

- Check Claim Settlement Ratio (CSR): Aim for 98%+ as per IRDAI data—don’t chase cheapest alone.

- Review Riders & Exclusions: Does your plan cover modern treatments like robotic surgery? Any waiting periods you can avoid by switching?

- Factor in Inflation: Ensure sum assured grows with medical costs (top-up plans help).

- Talk to Your Agent or Use Chatbots: Ask specifically why your premium rose.

- Run a Free Premium Calculator: Many portals have one—plug in details and see if you can save 10-30%.

- Renew or Switch Smartly: Portability rules let you switch health plans without losing benefits.

Do this once a year. It takes 30-45 minutes and can save thousands.

Desi Hacks to Lower Premiums Without Sacrificing Security

Here’s how to beat the 20% surge:

- Buy early—premiums rise with age.

- Opt for family floater for health (cheaper per head).

- Choose higher deductibles or super top-up for big savings.

- Maintain healthy lifestyle for “no-claim” discounts and lower loading.

- Pay annually instead of monthly to avoid extra charges.

- Combine term life with return-of-premium options if you want some money back.

- Leverage employer group policies as base, then top up personally.

- Review every renewal—don’t auto-renew blindly.

Wrapping It Up: To Pay More or Pay Smart?

Insurance premiums surging 20% in FY26 isn’t just news—it’s your wallet talking. For some, the hike is justified by rising costs and better coverage. For others, it’s a wake-up call to shop smarter. The difference lies in action: compare, question, and choose plans that fit your life, not the insurer’s bottom line.

If this blog made you pause and check your renewal notice, mission accomplished. Drop your story in the comments—did your premium jump this year? How did you handle it? Share tips, warn others, and let’s build a more insurance-aware India together. Your family’s future security starts with one click on a comparison tool. Don’t overpay—check today!

You May Like This

Advertisement

You May Like This

Advertisement

Advertisement

Advertisement